.svg)

Trauma Insurance

Written by

Hannah Lovegrove

Edited by

David Rayfield

Reviewed by

Adrian BennettCompare from a range of leading life insurance providers

iSelect’s partnered with Lifebroker to help you compare a range of Life Insurance policies. Not all policies are available at all times or in all areas. Any advice provided on this website is general in nature and does not consider your situation or needs. Please consider if any advice is appropriate for you before acting on it. Learn more.

What is trauma insurance?

Trauma insurance, also known as ‘critical injury’ or ‘recovery’ insurance, is a type of life insurance. It provides a lump sum payment if you’re diagnosed with a specific insurable injury or illness. This payment acts as a safety net, providing valuable financial support so you can focus on rest and recovery.

How could trauma insurance help you?

The lump sum, which is paid out as part of a trauma insurance claim, can be used at your own discretion and is commonly used to cover a range of expenses, including:

- medical costs not covered by your private health insurance

- any ongoing costs of treatment

- special transport requirements

- modifications to your house

- temporary loss of income.1For more information, see Moneysmart – Trauma insurance

What trauma insurance covers

When it comes to your trauma insurance payout, it’s up to you to decide how to use the payment. Whether you choose to put your payment towards out-of-pocket medical care, rehab costs, or to cover everyday expenses, this type of cover is there to provide financial support when you need it most.

Critical injuries

Most trauma insurance policies cover a range of injuries, such as severe burns or major brain injuries. Trauma insurance can also include cover for injuries leading to blindness, loss of hearing, or loss of a limb.

Critical illnesses

Cancer, heart attack, stroke, and coronary artery by-pass surgery are the four most common conditions covered by trauma insurance. The specific injuries and illnesses covered by trauma insurance will depend on your insurer and policy, so be sure to check your product disclosure statement (PDS) to understand exactly what you’re covered for.

How does trauma insurance help?

Helpful tip

Helpful tip

If you’re diagnosed with a serious health issue, you might try your best to limit its impact on your family and friends. But there’ll always be ripple effects on those closest to us. For instance, a loved one may have to cut back their work hours or step away from their job entirely to care for you. But a trauma insurance payout could reduce the impact on their lives financially. You might like to use the lump sum to help cover living expenses and additional support as you recover.

Adrian Bennett

General Manager for General Insurance

Trauma insurance explained, with iSelect

Learn more about how trauma insurance works in this short video.

Laura Crowden

ISELECT SPOKESPERSON

Frequently asked questions

How much trauma insurance will I need?

Before taking out trauma insurance, you’ll need to sit down and consider how much cover you’ll need. While most insurers will let you choose a benefit amount, exactly how much you need will depend on your individual situation.

To help you decide, it can be worth considering a range of different factors, like:

- how many dependents you have

- how much you owe towards your mortgage and other debts

- how much you have in savings and other investments

- whether you’ll have other financial support

- whether you have other insurance, like total and permanent disability (TPD) cover or income protection.

How much can trauma insurance cost?

Trauma insurance premiums differ from person to person. The cost of trauma insurance typically depends on several key factors, including:

- age

- gender

- medical history

- lifestyle

- coverage amount

- insurance provider.

What doesn’t trauma insurance typically cover?

There are a few key scenarios when you typically won’t be covered by your trauma insurance. Firstly, most insurers won’t cover an illness or an injury if it’s the result of an intentional, self-inflicted act. Secondly, most insurers will only pay benefits for an injury or illness that’s considered somewhat ‘severe.’ For example, broken bones won’t usually be covered, but loss of limbs would likely be considered an insurable event.

Will trauma insurance cover pre-existing conditions?

In the eyes of insurers, if you have a pre-existing medical condition, you’re often more likely to make a claim. With this in mind, insurers will often apply loadings or exclusions to account for the extra risk. A loading is a percentage increase that’s applied on top of the standard premium. On the other hand, an exclusion means that you’re unable to claim for an illness or injury that’s the result of an excluded pre-existing condition.

What kind of information will I need to give the insurer?

When it comes to taking out a trauma policy, you’ll often need to provide your insurer with personal details like:

- age

- job

- medical history

- family history

- lifestyle and smoking status

- high-risk sports, hobbies, or occupations.

In some instances, your insurer might also ask you to complete a medical assessment or request medical reports prepared by a doctor. If they don’t ask for this information, it could mean there are more exclusions listed in your policy or narrower policy definitions.

How is trauma insurance different from total and permanent disability (TPD) insurance?

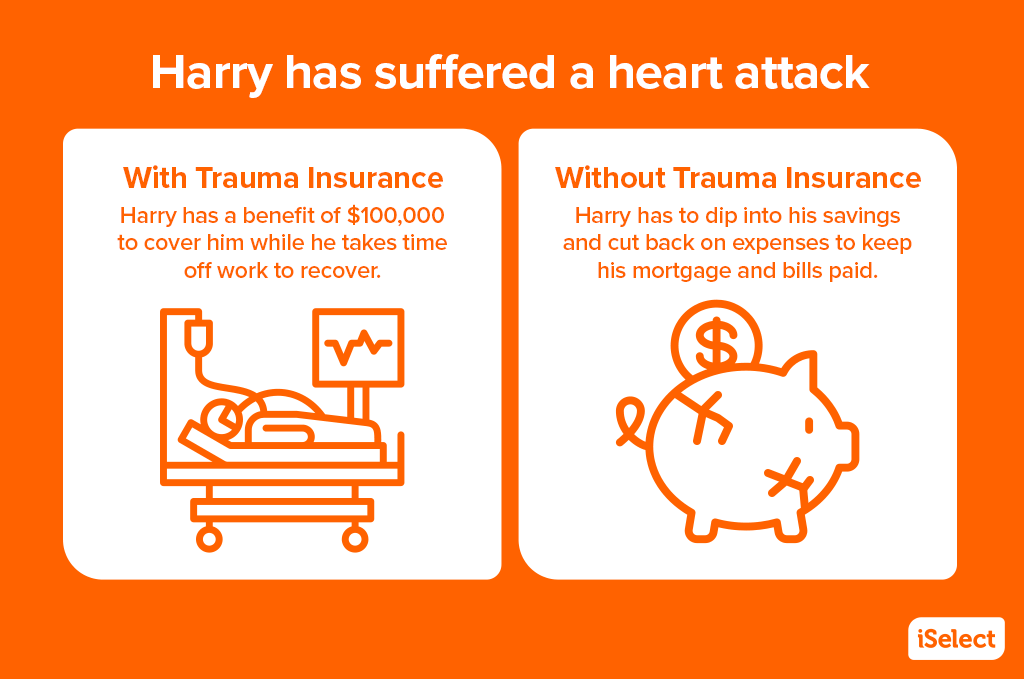

It can be easy to confuse trauma insurance with TPD cover and vice versa, but they are two different life insurance products. Trauma insurance provides financial support to help you recover from an illness or injury that isn’t permanently disabling. TPD insurance pays a lump sum in the event you become totally and permanently disabled because of an illness or injury and can’t return to work. For instance, trauma insurance can cover you while you take time off to recover from a heart attack or cancer, while TPD will cover you if you permanently can’t work due to your cancer diagnosis or heart attack.

What’s the difference between variable age-stepped and variable premiums?

In late 2024, life insurers introduced new labels for life insurance premiums. Instead of level and stepped premiums, life insurance premiums are now known as variable premiums and variable age-stepped premiums. Variable age-stepped premiums increase as you age, whereas variable premiums tend to be more stable over time.

With variable age-stepped premiums, cost of cover increases each year as premiums are based on your age at your policy anniversary. This is mainly because the likelihood of you making a claim increases as you age.

Variable premiums will usually be more expensive to begin with, but may work out cheaper in the long run. This is because the insurer calculates your premium based on your age when you take out the policy but then averages out this cost over a number of years.

How do I compare trauma insurance policies?

When it comes to comparing trauma insurance policies, you may want to carefully review a range of factors, including the cost, conditions covered, and waiting periods across different policies.

At iSelect, we’ve made it easy to compare trauma insurance policies by teaming up with our trusted partner, Lifebroker.

Easily compare life insurance quotes

Save time and effort by comparing life insurance from a range of policies and providers with iSelect’s trusted partner Lifebroker

iSelect’s partnered with Lifebroker (AFS Licence number: 400209) to help you compare a range of Life Insurance policies. iSelect earns a commission from Lifebroker for each customer referred through the website or contact centre. Lifebroker do not compare all life insurers or policies in the market.

iSelect Life Pty Ltd – ABN 89 124 304 347, AFS Licence Number 331128. Any advice provided by iSelect is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policies. You should consider iSelect’s Financial Services Guide which provides information about iSelect services and your rights as a client of iSelect.’