.svg)

Lenders Mortgage Insurance in Australia

Lenders Mortgage Insurance in Australia

Written by

Liv Steigrad

Edited by

Ellie Garran

Reviewed by

Sam HymanCompare home loans the easy way

We partnered with Aussie to help you compare home loans from over 25 lenders and over 2,500 home loan products.

What is lenders mortgage insurance (LMI)?

Lenders mortgage insurance, or LMI for short, is an insurance policy that gets tacked on to some home loans to protect the lender from losing money if the borrower defaults on their repayments.

It’s a one-off cost that the borrower has to pay, and it’s usually required when a lender thinks a borrower poses more risk – specifically, if their deposit is less than 20% of the property value.

When do you need to pay LMI?

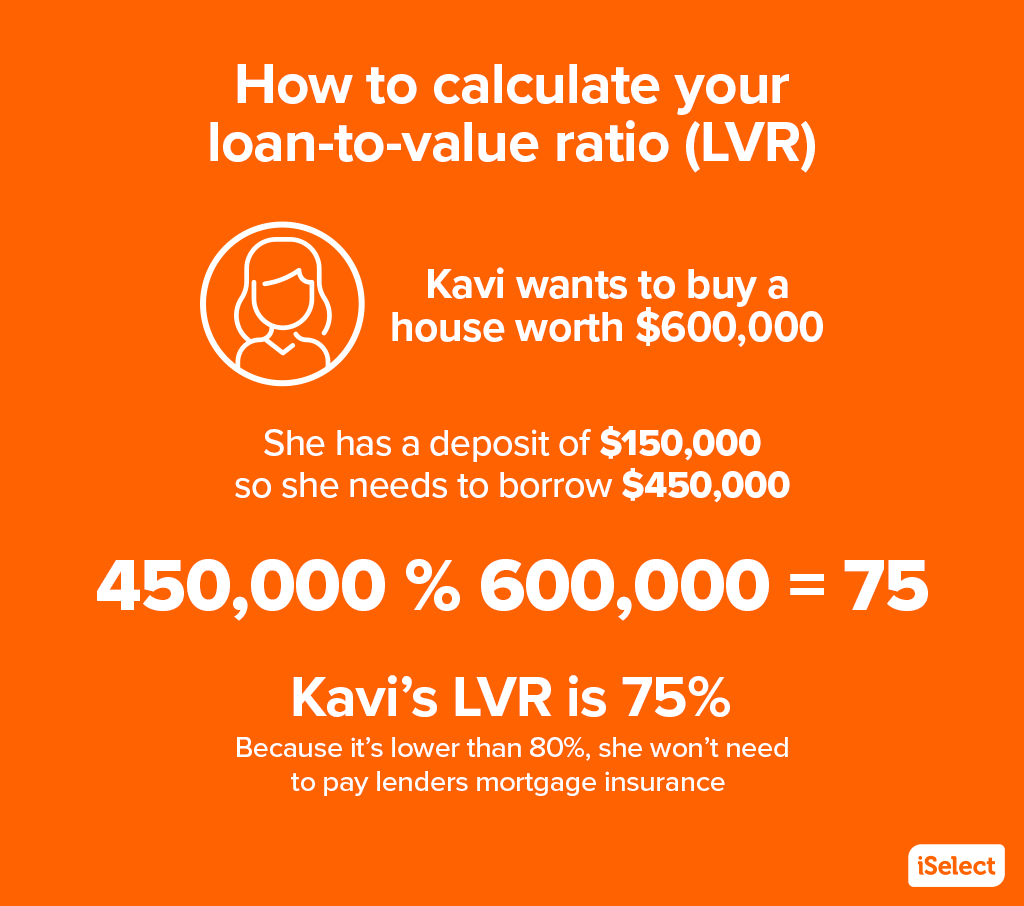

In general, banks work out whether to charge you LMI based on your loan-to-value ratio (LVR). This is what it sounds like: it’s a percentage figure calculating the proportion of your loan amount to the value of the property you’re buying.

If you’re putting down a deposit of 20%, your LVR is 80%. And if your LVR is higher than 80%, you’ll likely need to pay LMI.

Some lenders might waive LMI for people in professions that they consider less risky, including:

- medical professionals

- legal professionals

- accounting professionals

- media and entertainment industry figures

- athletes.

That being said, people in these professions will still need to meet specific requirements to get their LMI waived, and not all banks and lenders will necessarily offer the waiver.

How much does LMI cost?

Your actual LMI cost will depend on the value of your home and your LVR. It’s usually between 1% and 5% of your loan value. It can add up to thousands, or even tens of thousands, of dollars on top of your loan amount.

Unless you have the cash to pay your LMI up-front, it will likely get added to the total amount of your loan, which means you’d be paying interest on that extra amount too.

What factors can affect your LMI?

Your loan amount

Generally speaking, the more money you borrow, the higher the risk your lender is taking on. If you default on a repayment for a bigger loan, they’ll lose more money than if you default on a repayment for a smaller loan. Given that LMI is about protecting the lender from financial loss, higher risk tends to mean a higher LMI.

Your deposit amount

If you pay a relatively small deposit (anything less than 20%), then it’s likely you’ll be charged LMI. Again, this comes down to how much risk the lender would be taking with your loan.

Whether you’re an owner-occupier or an investor

Some lenders might charge more LMI for someone buying an investment property than for someone buying a home to live in. This is because lenders view investment as coming with more risks than a home purchase. Remember, not all lenders have the same policies around this, so it’s worth doing your research and asking questions while you’re shopping around.

Your profession

As we mentioned earlier, some banks will waive LMI for people who work in certain professions. These people still need to meet other requirements, so it’s a good idea to check with your lender to see what’s available to you.

Helpful tip

Helpful tip

When comparing home loans, it’s smart to ask each lender (or have your broker do it) to provide an estimate of their Lender’s Mortgage Insurance (LMI) premium. LMI costs can vary between lenders, so getting these estimates can helps you make better a well-informed decisions.

Sam Hyman

General Manager – National Sales, Aussie

What risks are associated with LMI?

Obviously, if you have to add LMI to your loan, your overall loan amount will be higher, which means you’ll pay more interest over time and your regular repayments will be higher.

The other important thing to know is that LMI is not transferable to another loan. That means if you refinance your loan and your LVR is higher than 80%, you might need to pay LMI for the second time.

Finally, if you default on your loan, you might still have to repay your LMI amount to your lender’s LMI provider. As you can imagine, this can be pretty tough if you’re already experiencing financial hardship. Luckily, for this reason, LMI providers have hardship provisions in place, such deferrals or instalment plans.

How can I reduce my LMI amount?

If your loan-to-value ratio is higher than 80%, there are a few things you can do to reduce or eliminate your LMI amount.

Keep saving until you can afford a 20% deposit

It’s not a fun answer, but the simplest way to avoid paying LMI is to keep saving until you can put down a 20% deposit on a property. Of course, you’d also need to weigh up the pros and cons of waiting longer until you buy your home.

Ask a parent or family member to be your home loan guarantor

LMI is automatically waived when you have a guarantor on your loan. A guarantor is somebody who agrees to be responsible for your loan if you can no longer afford it. It reduces the risk for lenders, but it passes the risk onto your family – it means they become liable for your loan.

Apply for the First Home Guarantee

The Australian Government’s First Home Guarantee allows eligible first home buyers to put down a lower deposit (as low as 5%). The government will then guarantee up to 15% of a deposit, allowing you to sidestep paying LMI.

Where can I find and compare home loans?

Here at iSelect, we’ve partnered with Aussie to make finding a great deal on your home loan as easy as pie. Get started comparing a range of lenders online, and figure out that pesky LMI once and for all.

Get started on comparing home loans today!

Find a home loan by comparing with iSelect’s trusted partner, Aussie.

iSelect is the trading name of iSelect Mortgages Pty Ltd (ABN 86 148 217 181). iSelect Mortgages Pty Ltd is a credit representative (Credit Representative 400540) of Lendi Group Distribution Pty Ltd (Australian Credit Licence 246786). iSelect provides a referral to Lendi Group Pty Ltd, a Credit Representative of Lendi Group Distribution Pty Ltd (Australian Credit License 246786). iSelect Mortgages Pty Ltd receives a commission from Lendi Group Distribution Pty Ltd, the licensee for each new customer account created and for each home loan submitted through this service.