.svg)

Mortgage Calculator

Mortgage Calculator

Written by

Luke Carlino

Edited by

David Rayfield

Reviewed by

Sam HymanCompare home loans the easy way

We partnered with Aussie to help you compare home loans from over 25 lenders and over 2,500 home loan products.

How do I use the Mortgage Repayment Calculator?

How do Mortgage Repayments Work?

How can repayment frequency affect my loan?

Can I pay off my loan faster with extra repayments?

Where can I find and compare Home Loans?

How do I use the Mortgage Repayment Calculator?

The Mortgage Repayment Calculator is a nifty tool for figuring out different home loan scenarios. Let’s say you’re eyeing a lovely house worth $750,000. You’ve got a cool $150,000 as a down payment (if you’re lucky!), which is 20% of the home’s price. The rest? That’s a $600,000 loan, covering the remaining 80% of the house. If you’re feeling bold, slash the loan term from 30 years to 25. Boom! You’re mortgage-free five years sooner, but brace yourself – your payments crank up a notch.

Punch in these details, and voila! The calculator shows you what your monthly payments might look like. You can switch it to show weekly or fortnightly payments–it’s your call.

Just remember, this calculator gives you ballpark figures. The real-deal costs, with all the fees, only roll in once you’ve wrapped up a full home loan application.

Helpful tip

Helpful tip

Whether you’re refinancing to lower repayments, access equity or tidy up your debts, start with a plan. Our mortgage calculator can give you a good snapshot of your repayments, but keep in mind that there could be lender fees or extra costs. So, always leave yourself a bit of breathing room. Numbers are a great guide, but don’t forget the real-world stuff that comes with them.

Sam Hyman

General Manager – National Sales, Aussie

How do Mortgage Repayments Work?

The biggest factor that determines your mortgage repayments is principal versus interest. To be clear:

Principal is the amount of money you borrow from the lender to buy your home.

Interest is the cost that the lender charges you for borrowing that money.

Different types of loans exist for a reason and you should choose the loan type most suited to your personal situation. A principal-and-interest loan is set up for you to pay for your home and lender costs at the same time – primarily so you can get rid of those interest payments, and your loan, sooner rather than later.

On the other hand, an interest-only loan exists to solely pay the interest (for a set period of time) while your actual home loan amount remains untouched. Why would anyone do this, you ask?

Well, interest only loans have lower regular repayments so if your situation isn’t financially stable right now, what you need today might be more important than worrying about tomorrow. Because you might have just had a child or you’re studying at university or … you just bought a house!

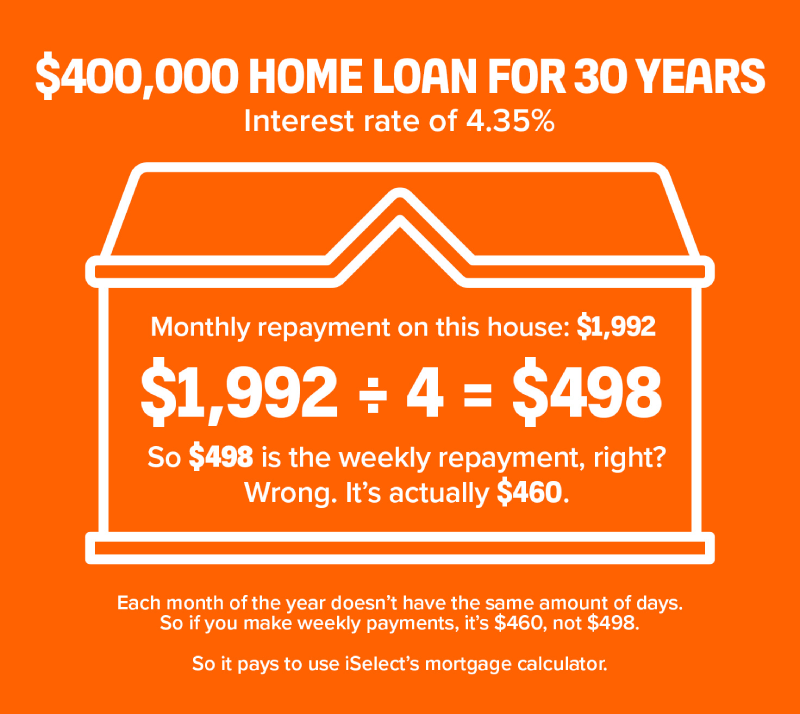

How can repayment frequency affect my loan?

Once you’ve signed on the dotted line and officially started having a mortgage, the rate of loan repayments might seem pretty straightforward. However, the Gregorian calendar (the one we’ve all used since 1582) has a few tricks up its sleeve.

There’s 12 months in a year, 26 fortnights and 52 weeks. But those fortnights and weeks might shake out differently when it comes to your repayments.

Take a look at our example.

Can I pay off my loan faster with extra repayments?

There’s millions of Australians who dream of the moment they make their final mortgage payment and own their home free and clear. It’s a strange concept to entertain because it seems like a long way off for so many people.

Paying off your loan faster with more payments? Well yeah of course, right? But we’re not all made of money. A mortgage repayment is hard enough to do as it is!

Hold on, there’s some good news. If you’re paying the previously mentioned $1,992 monthly instalment, you might think that’s your limit. That said, what if you throw a couple extra bucks on that? Maybe even ten?

Adding a small amount like $10 on your repayment amount can make a big difference. Using the iSelect Mortgage Calculator, it can save you $3,754 in interest and get you paying off your home loan three months earlier. All for the cost of a couple of Tim Tam packets.

Where can I find and compare Home Loans?

We’ve teamed up with the Aussie to hook you up with a whopping 2,500 home loan options.

Jump online to start comparing home loans today.

Get started on comparing home loans today!

Find a home loan by comparing with iSelect’s trusted partner, Aussie.

iSelect is the trading name of iSelect Mortgages Pty Ltd (ABN 86 148 217 181). iSelect Mortgages Pty Ltd is a credit representative (Credit Representative 400540) of Lendi Group Distribution Pty Ltd (Australian Credit Licence 246786). iSelect provides a referral to Lendi Group Pty Ltd, a Credit Representative of Lendi Group Distribution Pty Ltd (Australian Credit License 246786). iSelect Mortgages Pty Ltd receives a commission from Lendi Group Distribution Pty Ltd, the licensee for each new customer account created and for each home loan submitted through this service.