.svg)

Fixed vs Variable Home Loans

Fixed vs Variable Home Loans

Written by

Luke Carlino

Edited by

David Rayfield

Reviewed by

Sam HymanCompare home loans the easy way

We partnered with Aussie to help you compare home loans from over 25 lenders and over 2,500 home loan products.

What’s the difference between Fixed and Variable loans?

The basics of what makes a home loan ‘fixed’ or ’variable’ are actually pretty simple. A fixed interest rate is where your rate stays the same (at least for a certain period) while a variable rate can change with the market (i.e. Reserve Bank decisions).

| FIXED | VARIABLE |

| Essentially, a Fixed-Rate Home Loan is like locking in a deal. You agree with your lender on a specific interest rate and it remains constant for a set period—typically a few years. During this time, your interest rate and monthly repayments stay the same, giving you a predictable budget and peace of mind. There are also some restrictions on this loan type, like economic costs if you make extra payments, (such as early repayment fees) that are important to keep in mind. | Then there are Variable-Rate Home Loans which are a little more unpredictable. Their rates might start at a lower range than fixed loans, but they can also go up and down. Lenders can increase or decrease the interest rate attached to your loan based on market fluctuations, economic conditions, or their own policies. So, while you might enjoy a lower rate initially, there’s always the risk that your repayments could shoot up if the rates suddenly increase. |

The right choice will honestly depend on your own situation and what works with your budget and lifestyle. What’s most important is to make an informed decision because let’s face it, the average home loan will be part of your life for quite some time!

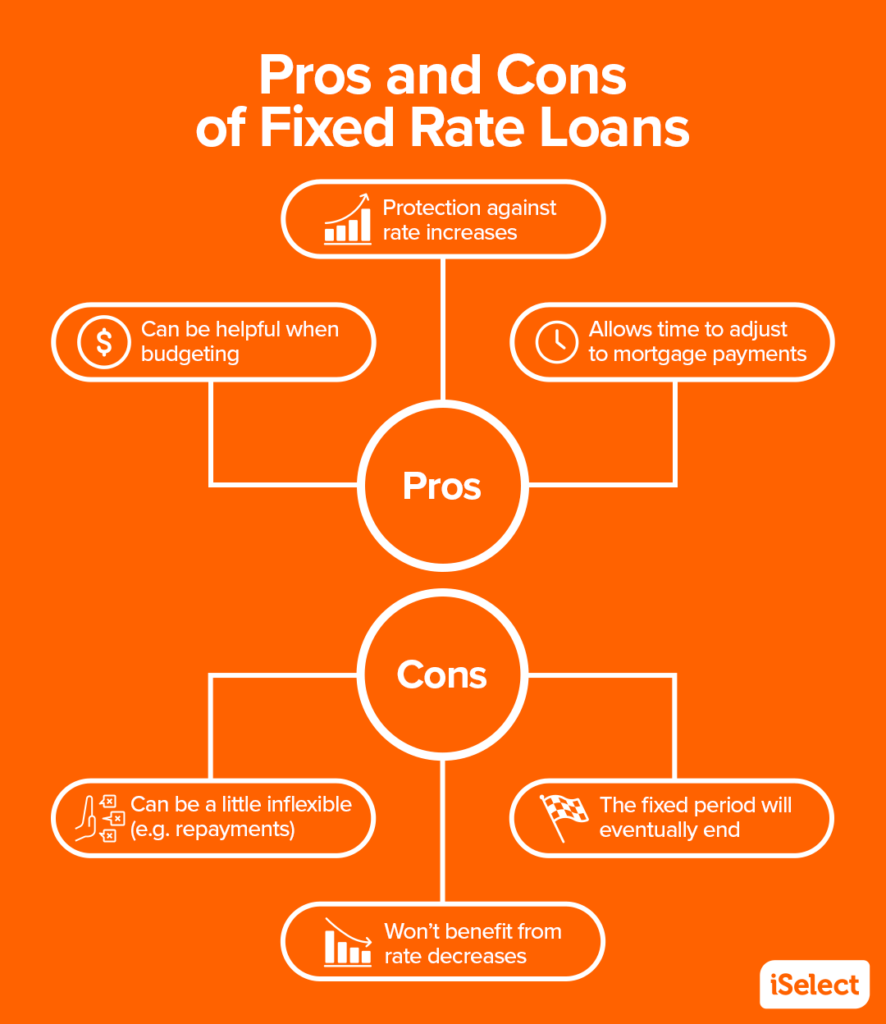

What are the pros and cons of Fixed-Rate Home Loans?

The safety and predictability of a fixed home loan can be great, but there are some downsides to consider. One of the most immediate effects of a fixed home loan can be on your budgeting. Knowing how much you’ll be paying with every instalment can make a huge difference in timing your payments as you won’t be affected by rate rises. But if rates go down, you won’t enjoy the reduced payments and keep in mind, fixed rates don’t last forever. Another drawback is that offset accounts usually aren’t available for fixed rate loans.

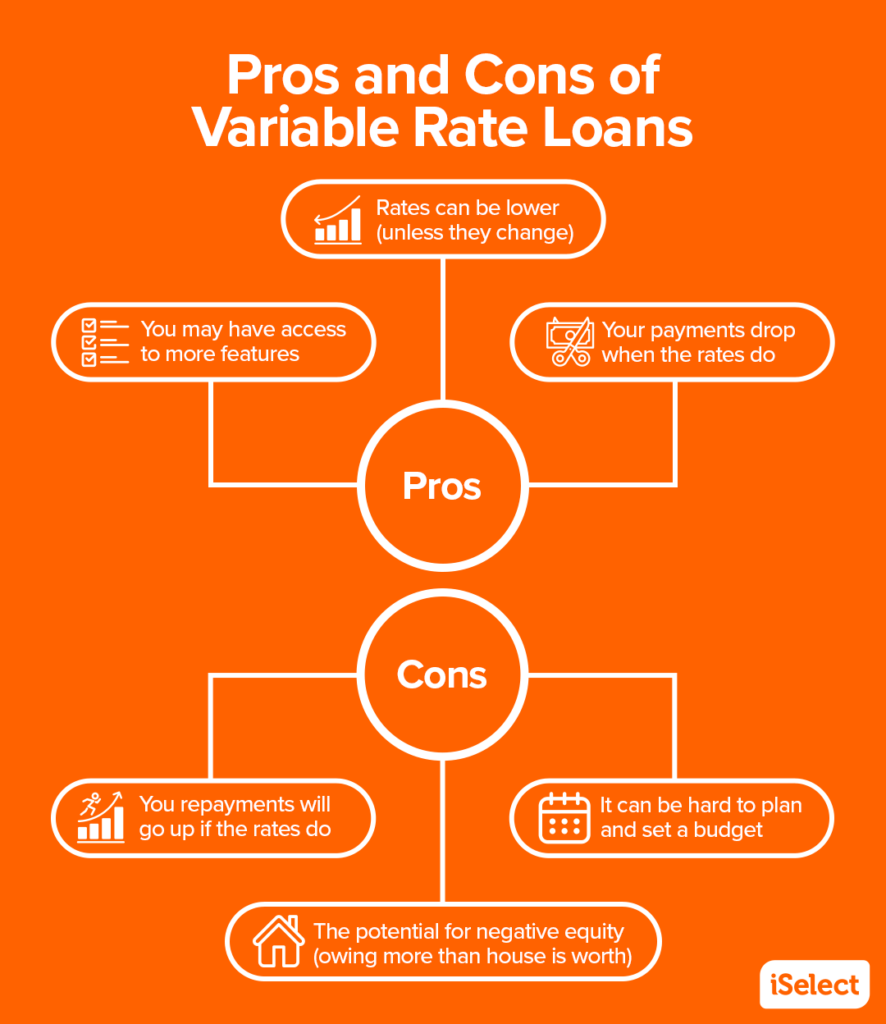

What are the pros and cons of Variable-Rate Home Loans?

Depending on the market, you could save a lot of money on a variable rate, but it might swing the other way as well. When the RBA drop interest rates, you’ll be happy because that means an easier time for you. On the other hand, budgeting could be much more unpredictable for the near future. Plus there’s a chance you’ll be impacted by negative equity.

One of the key advantages of a variable rate loan is the option to have an offset account. This handy feature means you can put your saving and spare cash in this account (which is linked to your mortgage account) to reduce the interest you pay. It can help you pay off your home loan sooner while giving you access to your money.

How can I tell which is best suited for me?

Figuring out the most suitable type of home loan when faced with the fixed vs. variable dilemma can be tricky. The key here is to avoid playing the guessing game about future interest rate movements. Instead, focus on your financial situation and what you can comfortably manage.

Take a good look at your budget, income, and expenses. Consider your long-term goals and the level of risk you’re comfortable with. If you prefer knowing how much you’ll pay each month and can handle a potential increase in interest rates, then a fixed-rate loan might be the better option for you.

On the other hand, if you’re comfortable with a bit of uncertainty and want the flexibility to benefit from lower rates if they occur (and that’s a big if), a variable-rate loan could be the way to go.

What about a Split Loan?

Some savvy borrowers can choose to hedge their bets by splitting their home loan. This means you don’t have to go all in with a fixed or variable loan. Instead, you can have the best of both worlds.

You pay a fixed rate on one portion of the loan, providing stability, and a variable rate on the other, offering flexibility. Say you have a loan of $600,000. Splitting the loan means you could have your overall loan, and loan type, broken into two. One fixed rate loan for $300,000 and then the other $300,000 has a variable rate. You can even divide them up differently to have a 60/40 split if you prefer.

It’s like having your cake and eating it, too – you enjoy the security of predictable repayments on one loan while taking advantage of potential rate drops with the other.

Can you switch Home Loan types?

Most banks offer the option to switch from a variable to a fixed home loan whenever you feel like it. However, changing your home loan may incur a number of payments such as rate lock fees or break cost fees.

Switching from fixed to variable isn’t quite so easy. Often, a fixed rate comes with a designated loan period as part of the deal. If you want to break that early to return to a variable rate (often because the rates have dropped), you may have to pay for it. Early repayment fees may be in the tens of thousands of dollars so check the fine print with your lender before making any decisions.

Where can I compare Home Loans?

We’ve teamed up with Aussie so you can easily explore various Home Loan providers in the market. Dive online to compare home loans effortlessly.

Get started on comparing home loans today!

Find a home loan by comparing with iSelect’s trusted partner, Aussie.

iSelect is the trading name of iSelect Mortgages Pty Ltd (ABN 86 148 217 181). iSelect Mortgages Pty Ltd is a credit representative (Credit Representative 400540) of Lendi Group Distribution Pty Ltd (Australian Credit Licence 246786). iSelect provides a referral to Lendi Group Pty Ltd, a Credit Representative of Lendi Group Distribution Pty Ltd (Australian Credit License 246786). iSelect Mortgages Pty Ltd receives a commission from Lendi Group Distribution Pty Ltd, the licensee for each new customer account created and for each home loan submitted through this service.