.svg)

Six Ways To Pay Off Your Mortgage Faster

Six Ways To Pay Off Your Mortgage Faster

Written by

Mel Basta

Edited by

Laura Crowden

Reviewed by

Sam HymanCompare home loans the easy way

We partnered with Aussie to help you compare home loans from over 25 lenders and over 2,500 home loan products.

Benefits of paying off your mortgage sooner rather than later

Buy a house — done.

Now that you’ve ticked off one of the most adult things to do (and after getting a photo with your partner next to the ‘SOLD’ sign), you’re now facing the inevitable: mortgage payments.

The thought of paying a mortgage over the next two or three decades can make you reach out for that Ventolin puffer or paper bag — whichever’s closer.

The good news is there are ways to trim years off your home loan, which also means you get to:

- save on thousands worth of interest throughout the life of your loan

- save more from overall borrowing costs

- cross the debt-free finish line sooner

Here are six tips to crush your mortgage ahead of schedule.

1. Perform an annual health check and consider refinancing

There are many things you can set and forget. Auto debit for utilities payments? Yes. Home Loans, probably not!

Home Loans need a little bit more love and attention. An annual health check is a great idea especially in a tight market because lenders will compete hard in getting (or keeping) you as a borrower.

See if you could revisit the refinancing costs and renegotiate your current rate with your existing lender. Are they offering better rates to new customers? If so, you might want to ask if they can pass you on to a lower rate too.

Note that lenders apply ‘loyalty tax’ to their existing borrowers. This means the existing borrower pays for interest rate typically higher than what new customers get. So just ask the question!

Also, have a look at your loan type.

Do you have a principal and interest or an interest-only home loan? Do you have a home loan with a fixed interest rate, variable interest, or a partially-fixed rate loan (also called split loan)?

If you’ve had your home loan for a while now, then you’re probably due for a revisit! And if you’re one of the many Aussie homeowners who’ve recently rolled off a pandemic low fixed rate of around two percent, then it’s definitely time to shop around!1Reserve Bank of Australia – Cash Rate Pass-through to Outstanding Mortgage Rates

Helpful tip

Helpful tip

Got a fixed home loan? Keep an eye on the end date.

When it ends, your rate could flip to your lender’s standard variable rate, usually higher than what’s available. That’s called a revert rate, and it can cost you more than you need to pay.

Stay ahead of the switch and shop around before it hits. Future-you will thank you.

Sam Hyman

General Manager – National Sales, Aussie

Each loan type has its pros and cons, which is why it’s a good idea to take the time to compare your Home Loan options or talk to an expert to gauge which suits your current (and future) circumstances.

2. Look into other lenders to land a better deal

If negotiating with your current lender doesn’t get you a better deal, explore your options and be prepared to vote with your feet. Moving to a new lender with a lower interest rate could significantly reduce your monthly repayments.

Compare what the big banks offer against smaller lenders. The latter sometimes gives options that the big guns don’t because they want to compete harder for you as a new borrower.

For example, smaller lenders tend to have lower interest rates and greater flexibility with their credit policies.

3. Increase your repayment amount

You could pay off your home loan faster by increasing your repayment amount.

If you’re able to switch to a lower-interest rate loan, keep paying the original amount (instead of lowering it to match the new rate) so you can pay down the principal quicker.

Send windfalls straight to the redraw facility! Say you get a performance bonus, land on top of your AFL tipping comp, or — in true highly-favoured-by-the-universe fashion — your dad transfers $10,000 into your account as a 30th birthday present.

Send them across as added contributions. They can compound to thousands of dollars and shed years off your Home Loan.

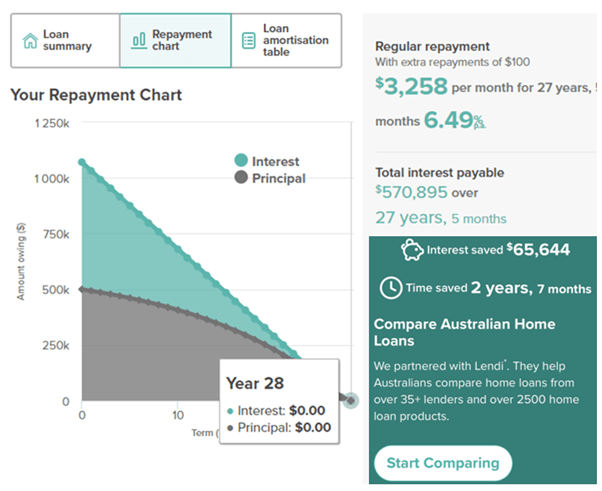

Too good to be true? Just look at the graph below.

Source: iSelect – Mortgage calculator

Our fictional couple Michael and Lee have decided to make an extra $100 in repayments on their Home Loan each month. They have $500,000 on their Home Loan and a 30-year loan term.

The graph shows us that at their current interest rate of 6.49%, their extra monthly contributions allow them to pay off the remainder of their home loan two years and seven months earlier than anticipated, saving them $65,644 over the term of their home loan.

Word of caution: Lenders have different rules around additional repayments, especially around redraw limits and steps. Some allow you to contribute added lump sums for a maximum number of times per year. Others have a limit on the amount you’re allowed to contribute. If you’re planning to increase your repayments, make sure to check with your lender first.

4. Pay more frequently

Consider making half of your monthly repayments every two weeks. Ask your lender if you can change the repayment frequency to fortnightly and if there are additional fees involved.

By doing this, you’ll make an extra month’s worth of repayments each year!

If Michael and Lee go from monthly repayments of $1,200 to fortnightly payments of $600, they’ll end up paying an additional $1,200 by the end of the year:

| Monthly | Fortnightly | |

| Amount | $1,200 | $600 |

| Frequency | 12 | 26 |

| Total | $14,400 | $15,600 |

| Difference (fortnightly vs monthly) | $1,200 | |

5. Take advantage of offset and redraws

Offset accounts and redraw facilities can bring down your borrowing costs and keep your cash flow in check. They help you save and maintain your liquidity at the same time.

Offset account

An offset account is a standard transaction account linked to your home loan, typically available in variable rate loans. You can use it for deposits and withdrawals like a typical debit card.

But here’s where offset accounts differ: They also let you bring down your monthly interest costs.

By using an offset, you get to apply the interest on your home loan on the net balance (your Home Loan balance minus your offset account balance). You’ll find that your lender — when determining your interest repayments — deducts the amount of money sitting in your offset account from the loan principal.

If Michael and Lee got $500,000 to pay off on their home Loan and they’ve put $10,000 in their offset account, then they’ll be charged interest on $490,000 on their home loan. This brings down their monthly interest costs.

If they both decide to keep the same repayment amount, then they’ll also pay down the principal.

Redraw facility

A redraw facility gives you the ability to access the money you’ve already put towards paying off a home loan.

Let’s say Michael and Lee can comfortably cover their monthly repayments and have made extra contributions from windfalls. If they have a redraw facility, they can access these repayments in case they need some extra cash for emergency.

Note that this isn’t offered across all loan types and lenders have different policies on redraw limits.

6. Prioritise your home loan

Freeing yourself from the mortgage monster means keeping your eyes on the prize. Tightening your belt on some of your less important expenses can add up to significant savings over time.

For example, make sure all your household services are working hard for you by comparing your electricity and gas, internet provider, or even your Health Insurance.

If making small cuts still won’t help, you can always talk to your lender and ask for advice on financial hardship.

Look into all your debts and tackle one at a time. Pay off the one with the highest interest first.

Compare Home Loans and find the fastest path to a mortgage-free life

iSelect has partnered with Aussie to help customers shave years off their Home Loan. Dash towards the debt-free finish line by comparing home loans from 25+ lenders online.

Get started on comparing home loans today!

Find a home loan by comparing with iSelect’s trusted partner, Aussie.

iSelect is the trading name of iSelect Mortgages Pty Ltd (ABN 86 148 217 181). iSelect Mortgages Pty Ltd is a credit representative (Credit Representative 400540) of Lendi Group Distribution Pty Ltd (Australian Credit Licence 246786). iSelect provides a referral to Lendi Group Pty Ltd, a Credit Representative of Lendi Group Distribution Pty Ltd (Australian Credit License 246786). iSelect Mortgages Pty Ltd receives a commission from Lendi Group Distribution Pty Ltd, the licensee for each new customer account created and for each home loan submitted through this service.