.svg)

Life Insurance for Families

Life Insurance for Families

Written by

Hannah Lovegrove

Edited by

Laura Crowden

Reviewed by

Eliza RyanEasily compare life insurance quotes

Save time and effort by comparing life insurance with iSelect’s trusted partner Lifebroker

What is family life insurance?

Family life insurance isn’t a specific policy type. But many people choose to take out life insurance for the purpose of protecting the financial security of their family should you pass away.

A term life insurance policy (also known as life cover or death cover) is designed to provide financial security for your partner and children in the form of a lump sum payment in the event you pass away or become terminally ill. Ultimately, life cover can help ensure your loved ones in the unfortunate event of your death by helping to cover expenses like mortgage repayments, living costs, education fees and other family needs.

What expenses can term life insurance cover for your family?

Term life insurance acts as a financial safeguard for families in case either or both income earners pass away. Losing a partner or parent can be incredibly distressing. But if you have taken out an appropriate life insurance policy, your family hopefully won’t have to worry as much about the immediate costs of your death or diagnosis, as well as ongoing living expenses.

Immediate costs can include:

- One less income to support the household

- Funeral expenses

- Hospital expenses before death, if diagnosed with a terminal illness

How much coverage will I need to support my family?

The amount of life cover you may need to protect your family depends on your situation and your budget. As a general rule, a higher coverage policy will generally result in higher premiums.

Ongoing expenses can include:

- Childcare and schooling expenses

- Food and clothing

- Mortgages, loans and household bills

- Home help for household duties

It’s always worth considering what kind of expenses your family will need to cover to maintain their current lifestyle, along with what debts will need to be repaid.

Before you take out a policy, be sure to consider a range of factors that are unique to your family, like:

- Your financial situation – both current and future

- The age of yourself and your partner

- Your employment situation and your partner’s

- Contributions to things like household expenses, debts and savings

- The number of children in your family

- How many years you’ll need to cover your children

- Your assets and superannuation funds

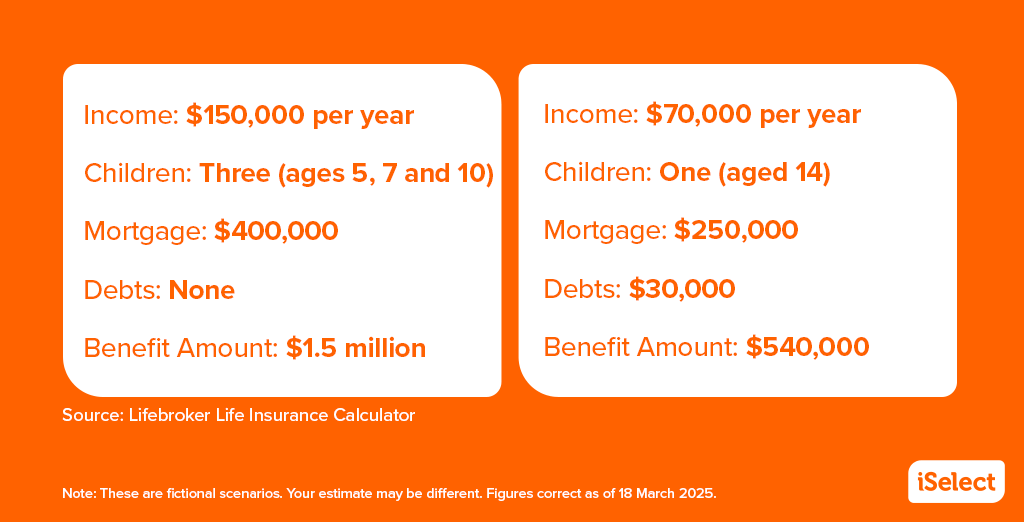

The example below shows how different families might come to different conclusions when it comes to deciding how much life insurance coverage they need.

How much could term life insurance premiums cost your for family?

The cost of life insurance premiums will differ from one family to the next. Insurers calculate the premiums based on a range of factors, such as:

- The number of people insured, including parents and children

- The age, health, lifestyle (e.g. smoking status) and occupation of those being insured

- The level of cover

- Benefit amount

- Premium structure (i.e. stepped vs level premiums)

To give you a rough idea of cost, a term life insurance policy with $1,000,000 of cover may, on average, initially start at $27 per month for a 35-year-old non-smoking female and $34 a month for a 35-year-old non-smoking male.1Figures calculated using Lifebroker’s service on 25 March 2025 for a 35-year-old woman and man who don’t smoke, live in Melbourne (postcode 3000), and work generic white collar roles. These figures are rounded to the nearest dollar amount and are examples only. Your results may be different. These premiums typically increase based on the number of people added to the policy.

When should you take out life insurance to protect your family?

Helpful tip:

Helpful tip:

There’s no wrong time to take out life insurance, but there are certain times during your lifetime that it might be more relevant to consider taking out life insurance for the first time, or reviewing your cover. Major life milestones such as getting married, buying a house (and getting a mortgage) and starting a family are all common trigger points for considering your life insurance options.

Eliza Ryan

Senior Marketing and Growth Channels Manager, Lifebroker

What kind of insurance can I get for my family?

There are a number of different types of life insurance policies you can take out to suit the needs and budget of your family. Just be sure to consider your family’s individual circumstances when choosing a provider and a policy.

Confusingly term life insurance is just one type of life insurance. Here’s a quick breakdown of some of the most common life insurance policies.

Life insurance

Term life insurance (also known as life cover or death cover) provides cover in the event of death or the diagnosis of a terminal illness. If either of these insurable events occur, your beneficiaries, which you may assign to family members, could be eligible for a lump sum payout, which is typically tax-free.

Children’s insurance

Children’s insurance covers cases where a child passes away or is diagnosed with a terminal illness. Children’s insurance is typically offered as an optional extra on top of most life insurance policies. Like life insurance, it’s paid as a lump sum payment and can cover additional medical and educational expenses.

Total and permanent disability (TPD) insurance

TPD insurance provides cover in the event you’re totally and permanently disabled due to illness or injury. Once again, TPD is a lump sum payment that can be used to cover a range of expenses.

Critical illness insurance or trauma insurance

Trauma insurance provides a lump sum payment if you’re diagnosed with a specified insurable illness or injury., Trauma insurance is meant to provide financial support throughout your recovery and rehabilitation.

Income protection insurance

While plenty of us wish we didn’t need to work, the reality is that we need a regular income coming in. Income protection insurance can help you stay on top of regular bills if you can’t work by paying a portion of your salary.

How to find suitable life insurance for you and your family?

When it comes to comparing life insurance policies to find the most suitable option for your family, you’ll need to consider several different factors. Have a read of the Product Disclosure Statement (PDS) and ask yourself:

- What conditions are covered? Check if the policy will exclude any pre-existing conditions or place on loadings.

- How much can I get insured for? Insurers often apply limits to the benefits paid.

- How much do the premiums cost?

- What are the waiting periods?

- Will the premiums increase with indexation?

If you already have your own life insurance policy, it could also be worth checking to see if you can add your children. Some insurers will allow you to add children to a pre-existing singles policy for an additional cost.

Looking for a life insurance policy? Compare with Lifebroker

Whether you’re expecting your first child or adding a new addition to the family, family life insurance can provide peace of mind and financial security. At iSelect, we’ve teamed up with Lifebroker so you can easily compare family life insurance policies from some of Australia’s most trusted insurers.

Easily compare life insurance quotes

Save time and effort by comparing life insurance from a range of policies and providers with iSelect’s trusted partner Lifebroker

iSelect’s partnered with Lifebroker (AFS Licence number: 400209) to help you compare a range of Life Insurance policies. iSelect earns a commission from Lifebroker for each customer referred through the website or contact centre. Lifebroker do not compare all life insurers or policies in the market.

iSelect Life Pty Ltd – ABN 89 124 304 347, AFS Licence Number 331128. Any advice provided by iSelect is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policies. You should consider iSelect’s Financial Services Guide which provides information about iSelect services and your rights as a client of iSelect.’