.svg)

Green Slip Car Insurance

Green Slip Car Insurance

Written by

Kervin Mathew

Edited by

Ellie Garran

Reviewed by

Toby HagonCompare car insurance policies the easy way

Save time and effort by comparing a range of car insurance quotes with iSelect

What is Green Slip/CTP car insurance?

Long story short

Green Slips are mandatory

You need a Green Slip (CTP insurance) to register and drive legally in NSW. Without it, you could face steep medical costs for accident-related injuries.

You can pick your own provider

The NSW Government lets you compare Green Slip providers. All policies include the same base coverage but might offer unique incentives.

Green Slip costs vary

The average Green Slip in NSW for 2024 cost $494.1NSW Government State Insurance Regulatory Authority – 2017 CTP Scheme Open Data But your age, driving record, and car type, among other factors, can nudge the price up or down.

A Green Slip covers costs related to injury

This includes medical bills, lost wages and even help around the house for up to a year, or longer if the accident wasn’t your fault.

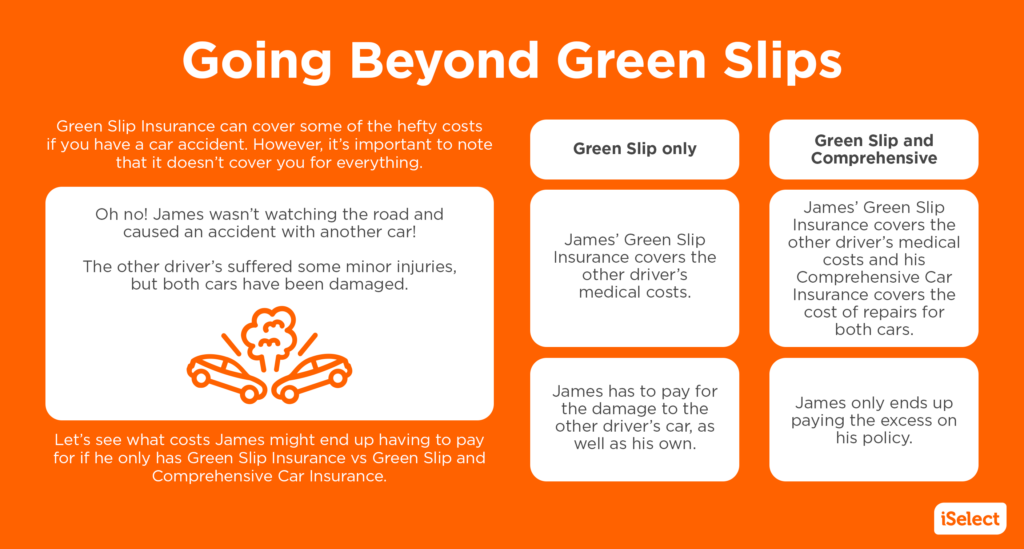

It doesn’t cover car repairs or property damage

For that, you’ll need a top-up such as comprehensive or third-party property.

What is Green Slip/CTP car insurance?

A Green Slip is a car insurance policy that helps provide compensation for people killed or injured in a motor vehicle accident. Whether it’s called a ‘Green Slip’ or CTP insurance, it’s important to know what it covers. Why? Because if you own a car, you must also have a minimum level of car insurance.

That’s right – everyone in Australia needs to have some kind of compulsory third party (CTP) insurance before they can get on the road. In NSW, it’s called a Green Slip.

Without a Green Slip, you might be required to pay for an injured person’s medical costs (among other things!) if the accident is your fault. These costs can be quite high, ranging from thousands to even hundreds of thousands of dollars.

Green Slip insurance explained

Learn what a Green Slip is, why you need it in NSW, what it covers, and its limitations.

Are Green Slips compulsory in NSW?

Yes. You need a Green Slip to register and legally drive your vehicle in NSW.

Where can I compare CTP Green Slip insurance?

The NSW Government’s State Insurance Regulatory Authority (SIRA) lets you compare Green Slip insurance quotes.2For more information, see State Insurance Regulatory Authority – Green Slip

NSW drivers need to choose their own Green Slip insurance provider before they register their vehicle. There are currently six licensed insurers who offer Green Slip insurance policies.

Bear in mind that a Green Slip won’t cover the repair costs of your or anyone else’s vehicle, nor any property damage. You’ll need a higher level of car insurance for that.

Helpful tip:

Helpful tip:

Car insurance is a great way to protect yourself, but there are a lot of other ways that you could prevent accidents from even happening in the first place. A car with great safety features such as cameras, blind spot warning systems, and autonomous emergency braking can assist the driver if they make a mistake. But not all advanced driver assistance systems are created equal, so make sure you do your research when buying a new car – and test the technology on roads you’re familiar with before signing on the dotted line.

Toby Hagon

Motoring Journalist

How much does a Green Slip cost?

Insurers follow a set price range for Green Slip insurance, but the price can still differ depending on your and your vehicle’s risk level. There are a few things that can influence this, such as your age, any demerit points you have, your claims history, the age of your vehicle, where it’s kept, and whether it’s covered by comprehensive insurance.

The average Green Slip premium for 2024 is $494.3NSW Government State Insurance Regulatory Authority – 2017 CTP Scheme Open Data How much you end up paying can also depend on the type of vehicle you drive and where in NSW you live.

What does Green Slip/CTP insurance cover?

Green Slip insurance typically covers anybody who gets injured in a road accident, regardless of who was at fault (unless you’re charged with a dangerous driving offence). You’ll usually get to claim up to a year of the following:

- a portion of your pre-injury weekly income if you need to take time off work

- necessary treatment and rehabilitation expenses

- at-home support services if you need help around the house while you recover.

If you find yourself seriously injured after being involved in an accident that wasn’t your fault, you may also be able to claim benefits beyond one year.

On top of this, anyone injured by your vehicle is generally covered by your policy. This usually includes the following:

- you, your passengers, or anyone else driving or riding in your vehicle

- the drivers, passengers, and riders of any other vehicles that are injured by your vehicle in the accident

- cyclists, pedestrians, and other road users that are injured by your vehicle

What is generally not covered by Green Slip insurance?

Green Slips don’t cover the cost of vehicles or property that are damaged in an accident. For this kind of cover, you might consider looking into other insurance types, like comprehensive, third-party property and third-party fire and theft.

Frequently asked questions

Does it matter what insurer I choose to go with?

All Green Slips give you the same, basic level of protection. However, some insurers will offer additional types of cover and incentives, so it’s always a good idea to check out what’s included in the policy and how much cover you’ll get. Once you’ve purchased your policy, your chosen insurer will then work with NSW’s State Insurance Regulatory Authority to sort out your car registration.

At iSelect, we don’t compare Green Slip car insurance, but when it comes to additional cover, such as third party property, third party fire and theft, and comprehensive, we can help. Start comparing from our available policies and providers.

Are there different types of Green Slip/CTP insurance?

Generally, there are two different types: either a 6-month or 12-month policy. The only other options are available to motor dealers and fleet owners. However, if you drive a historic vehicle, a purpose-built vehicle, or any other limited road access vehicle, you might only be required to get a conditional registration or an unregistered vehicle permit.

If I have an accident in a different state, am I still covered by Green Slip insurance?

Yes, Green Slip insurance insures NSW drivers all over Australia no matter where the accident occurred, even if it was on private land. However, some states and territories will not cover your medical costs if the accident was your fault. This is the case for South Australia, Western Australia and Queensland – although exceptions might be made depending on the severity of your injuries.

What happens if my Green Slip expires?

If your Green Slip expires, you need to organise a new one to be able to register your car. If you renew your Green Slip after the due date, make sure you wait until you’re covered to get on the road, or you could be fined.

Are there situations where I can get a refund on my Green Slip?

You might be able to get a partial refund. However, this will depend on your insurer – and even then, it’s usually only when your car becomes unregistered.

The registration will have to be cancelled for specific reasons, too. This might be because it gets ‘written off’, which means it’s so damaged that it would cost more to repair than to replace. Or because it gets stolen. Or if you get it scrapped at an auto-wrecker.

You can also cancel your car’s registration at a Service NSW Centre. However, you’ll want to speak to your insurer and find out if you’re even eligible for a refund in the first place. Typically, they’ll also ask for a letter or receipt that shows when the registration was cancelled.

What happens if I sell my car?

Just like the registration, the Green Slip stays with the car and is transferred when the registration is transferred. In many instances the new owner may have different circumstances – including their postcode and crash risk – but that will not change the premium until it is renewed.

What information do I need to give my insurer when organising a Green Slip?

Honesty is the best policy. When buying a Green Slip, it’s important to give accurate information about your vehicle, yourself, and anyone else who might be driving your car. Your insurer will most likely ask for the following information:

- the year you bought your car

- the make and model of your car

- the age of anyone who might drive the car

- any demerit points you or other drivers have

Looking for additional cover on top of your Green Slip? Compare quotes with iSelect

At iSelect, we can help you explore third party and comprehensive car insurance policies from our range of providers. Use the iSelect car insurance comparison tool to get started.

Get started on comparing car insurance policies!

Save time and effort by comparing a range of car insurance quotes with iSelect

iSelect General Pty Ltd (ABN 90 131 798 126. AFSL 334115) has partnered with Compare the Market (ABN 83 117 323 378. AFSL 422926) to compare a range of car insurers and policies. Not all providers in the market or all policies offered by the partners are compared and not all policies or special offers are available to all customers.

A number of our participating general insurance brands are arranged by Auto & General Services Pty Ltd ACN 003 617 909 on behalf of Auto & General Insurance Company Limited 111 586 353, both of which are related entities of iSelect Limited. Our relationship with those companies does not impact the integrity of our comparison service. Click here to view iSelect’s range of providers.

Any advice provided by iSelect is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policy. You should consider iSelect’s Financial Services Guide which provides information about our services and your rights as a client of iSelect. iSelect receives commission for each policy sold that is a percentage of the premium or a flat fee. Ask us for more details before we provide you with any services.