.svg)

Windscreen Cover and Excess

Windscreen Cover and Excess

Written by

Kervin Mathew

Edited by

Laura Crowden

Reviewed by

Adrian BennettCompare car insurance policies the easy way

Save time and effort by comparing a range of car insurance quotes with iSelect

What is windscreen cover?

Long story short

Windscreen cover can save you money

Windscreen insurance cover is a common optional extra with comprehensive car insurance policies that could potentially save you up to a $1000 or more if your windscreen is damaged.

Pay lower or no excess on claims

With windscreen cover, you can claim window repairs or replacements with a reduced or zero excess. Some insurers may even allow unlimited windscreen claims per year.

Driving with a damaged windscreen can be illegal

In Australia, windscreen damage above certain limits – such as above 150mm – can make your car unsafe and illegal to drive.

What is windscreen cover?

Windscreen cover is a common type of optional extra with car insurance. It helps either lower or completely waive the excess for claims related to repairing or replacing windscreens or car windows.

Whether it’s fixing a tiny chip or a large crack, windscreen cover can save you hundreds of dollars in repairs or replacement costs.

Windscreen insurance cover is sometimes also referred to as reduced window glass excess, windscreen and window glass cover or excess free windscreen cover.

Is it worth getting windscreen cover?

It really depends on your driving habits. If you drive often or park in areas peppered with road debris, windscreen cover would likely be a very sensible addition to your car insurance policy because your windscreen is more exposed to the risks that can cause it damage.

However, if you’re a casual driver or you have a basic windscreen without high-tech features like lane assist, you may decide to go without it and simply accept that you’ll need to pay up front for any window repairs if they are ever needed. It all comes down to balancing the level of risk you are comfortable with and the cost you can afford.

Pros and cons of having windscreen cover

| Pros | Cons |

How does windscreen cover work?

When you take out car insurance, you might be able to add windscreen insurance cover for an additional cost. Windscreen cover is commonly offered as an optional extra with comprehensive cover, although some higher-tier policies may include it as standard. Some windscreen cover options offer a reduced excess for window repairs, while others waive the excess on window repairs entirely.

If you’ve added windscreen cover to your policy, and your windscreen or car windows are damaged and need repairing or replacement, then you won’t have to pay the full standard excess on your car insurance policy. Without window cover, you would either have to choose between paying your policy’s full excess or opting to pay for any repairs yourself in full without claiming on your car insurance.

Some insurers offer unlimited claims under their windscreen cover. Others may limit it to one windscreen claim per year only, with any additional claims incurring the standard excess that comes with your car insurance policy.

As the name suggests, windscreen cover only works only if the damage to your car is limited to windows and windscreens. A claim that includes additional damage, say broken mirrors or headlights, may mean that you will be required to pay your policy’s full standard excess.

How much does windscreen cover cost?

Because windscreen cover is generally an optional extra, this means it usually comes at an additional cost which will hike up your overall premium. Insurers consider a range of factors when deciding how much it will cost to add windscreen cover to your policy.

Car type

Luxury or rare vehicles often feature expensive parts or ones that are hard to come by – windscreens are no exception.

Driving habits

Frequent driving on the highway or on unfinished roads with loose stones and gravel can increase the risk of windscreen damage.

Location

Living in an area known for traffic, extreme weather or a high occurrence of crimes like vandalism may mean higher premiums.

Your insurer

Higher-tier policies that offer unlimited windscreen repairs typically have a higher price point.

Is it illegal to drive with a damaged windscreen?

It may be a brag to say that you’re able to do certain things with your eyes closed. Driving is not one of them. In the same vein, driving with a windscreen that impairs your view can be unsafe and even illegal. The size and position of the damage on your windscreen will largely decide whether you’re driving legally or not – as will your respective state or territory laws.1For more information, see National Transport Commission – Australian Road Rules

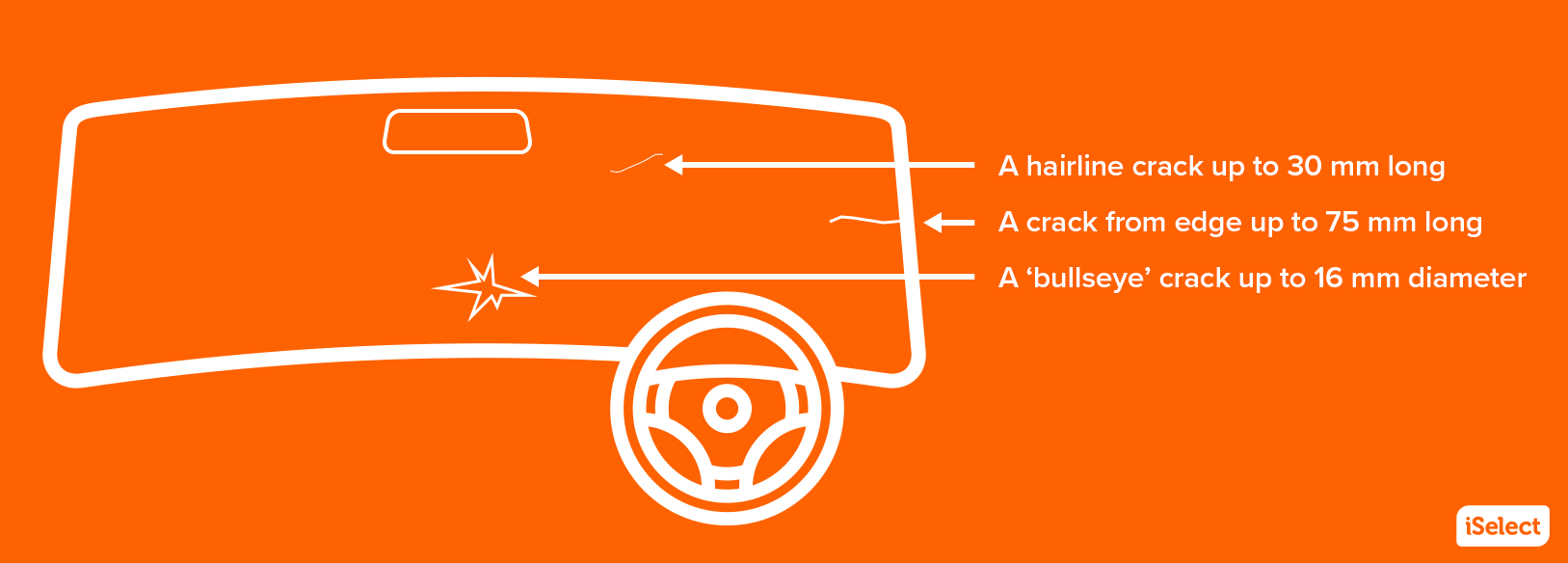

As a rule of thumb, the driver’s side of a windscreen must be free from:

- star or bulls-eye fractures bigger than 16 mm in diameter

- hairline or straight-line cracks that exceed 150 mm (or more than 30 mm in ACT and NSW)

- cracks deeper one layer of laminated glass.

How do I make a windscreen cover claim?

Say you’re driving on a motorway, and out of nowhere you hear a faint yet menacing ‘clink’. Eventually, you notice a small crack on your windscreen. Before you start asking yourself, ‘Why me?’, you remember that you signed up for windscreen cover with your car insurance policy!

Here’s how a scenario like this might play out.

- You get online or on the phone with your insurer to tell them what happened and lodge a claim.

- Your insurer or a repairer within your insurer’s network should get in touch to let you know what happens next.

- You’ll discuss things like location and the extent of the damage, and arrange a time and place for repairs or replacement.

If the damage is minor, a repairer could quickly restore your windscreen or window glass. If the crack is big enough to obstruct the driver’s view, a full replacement might be necessary.

Remember, it may be illegal to drive a car with a significantly damaged windscreen. In this case it may be better to play it safe and find alternative transport until your car is safe to drive or discuss getting a tow with your insurer.

Helpful tip:

Helpful tip:

With optional windscreen cover on your comprehensive policy, you needn’t have to think twice about getting your windscreen fixed – saving you not only the repair cost but also potentially hundreds in fines and, worse still, the hassle of a nasty bingle due to impaired vision.

Adrian Bennett

General Manager for General Insurance

Frequently asked questions

How much does it cost to repair or replace a windscreen?

The cost to repair or replace a damaged windscreen depends on the extent of the damage and the car you drive. While a small chip may only cost around $100 to repair, more extensive repairs or a full replacement can easily cost a thousand dollars or more.

Luxury cars or vehicles which feature advanced driver assistance systems (ADAS) such as rain sensors or a heads-up display (HUD) generally cost more to repair or replace.

Is windscreen cover always an optional extra with car insurance?

Usually, yes. Windscreen cover is generally offered as an optional extra with comprehensive car insurance and sometimes even third-party fire and theft policies. Some insurers may offer it as a standard inclusion with higher levels of comprehensive cover.

The reason it’s usually an optional extra is that some drivers may prefer to pay more for the extra protection and peace of mind that windscreen cover provides, while others may choose to opt out to keep premium costs down.

Is windscreen cover only available with comprehensive cover?

No, but it’s more commonly offered as an optional extra with comprehensive policies (and only found as a standard inclusion on a limited number of higher-tier comprehensive policies).

Some insurers do offer excess free windscreen cover as an optional extra with their third party fire and theft policies but generally your windscreen cover options are more limited with lower levels of car insurance.

When considering optional extras like windscreen cover, always be sure to read through the product disclosure statement (PDS) so you’re clear on what’s covered under a policy.

Am I still covered for a cracked windscreen without windscreen cover?

Yes. Generally, a comprehensive or, in some cases third-party fire and theft policy, will still cover windscreen damage even if you don’t have windscreen cover. The difference is that without windscreen cover, you’ll have to pay your policy’s standard excess, which is likely much higher than the reduced or zero excess that comes with windscreen cover.

And even if your policy does include windscreen repairs, without windscreen cover it may not be worthwhile claiming minor windscreen repairs on your insurance. That’s because your policy’s standard excess might cost more than simply paying the windscreen repair cost yourself upfront.

Does windscreen cover include damage to sunroofs and side mirrors?

Yes. Typically, windscreen cover will cover damage to all your car windows – that means your front windscreen, any side windows and back windows. Windscreen cover under some policies might even extend to include sunroofs.

As always, it’s important to read the PDS to understand exactly what’s covered and what’s not.

Does windscreen cover include side mirrors?

No, generally not. Windscreen cover doesn’t usually cover you for damage or repairs to side-view and rear-view mirrors or headlight lenses and indicator glass.

Want to add more value to your insurance with optional extras?

Give the iSelect comparison tool a go to explore our range of policies with windscreen cover as an optional extra, along with other potentially valuable add-ons.

Get started on comparing car insurance policies!

Save time and effort by comparing a range of car insurance quotes with iSelect

iSelect General Pty Ltd (ABN 90 131 798 126. AFSL 334115) has partnered with Compare the Market (ABN 83 117 323 378. AFSL 422926) to compare a range of car insurers and policies. Not all providers in the market or all policies offered by the partners are compared and not all policies or special offers are available to all customers.

A number of our participating general insurance brands are arranged by Auto & General Services Pty Ltd ACN 003 617 909 on behalf of Auto & General Insurance Company Limited 111 586 353, both of which are related entities of iSelect Limited. Our relationship with those companies does not impact the integrity of our comparison service. Click here to view iSelect’s range of providers.

Any advice provided by iSelect is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policy. You should consider iSelect’s Financial Services Guide which provides information about our services and your rights as a client of iSelect. iSelect receives commission for each policy sold that is a percentage of the premium or a flat fee. Ask us for more details before we provide you with any services.