.svg)

Classic and Vintage Car Insurance

Classic and Vintage Car Insurance

Written by

Tina Sendin

Edited by

Laura Crowden

Reviewed by

Adrian BennettCompare car insurance policies the easy way

Save time and effort by comparing a range of car insurance quotes with iSelect

What is classic and vintage car insurance?

Long story short

Specialised coverage exists for classics

Classic and vintage car insurance offers tailored protection, covering agreed value, limited use, and restoration needs for collectible vehicles.

Some insurers define ‘classic’ or ‘vintage’ differently

Your car must meet your insurer’s definition of ‘classic’ or ‘vintage,’ which is often based on age – usually 15+ years for classics and 40+ years for vintage.

Classic and vintage cars can come with more risks

Classic cars can pique the interest of thieves. Plus, they’re more costly to repair and usually lack modern safety features – making specialised insurance a smart move.

Premiums vary depending on different factors

Costs depend on factors like age, usage, and condition. Limited use and agreed value policies can reduce premiums while ensuring full coverage.

What is classic and vintage car insurance?

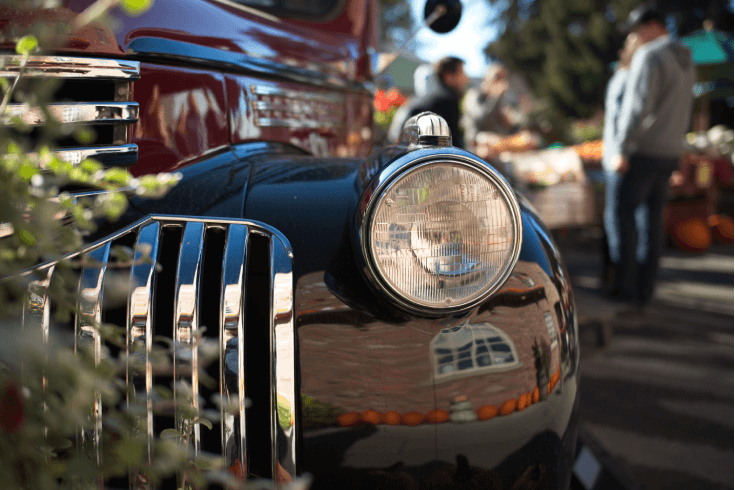

Owning a classic or vintage car is like having a precious heirloom parked in your garage. These cars are craftsmanship, nostalgia, and old-school charm on wheels. But as much fun as it is to show off your pride and joy, they come with unique qualities and risks that an average car insurance policy may not cover.

Classic and vintage car insurance offers specialised coverage tailored to the unique needs of collectible vehicles. These prized possessions are typically driven for recreational purposes, rather than everyday use.

Classic and vintage car insurance goes beyond the basics. Its bespoke coverage attracts car enthusiasts with perks like club plate and limited use cover, as well as laid-up cover for restoration projects.

Since classic and vintage cars are one of a kind, some insurers let you customise your coverage to match how often you drive them.

What makes a car vintage or classic?

The terms ‘classic’, ‘vintage’, and ‘modern classics’ can be confusing, but car insurers treat them as separate categories. The tricky part? There’s no standard definition – each insurer classifies these cars differently, often by their age:

- Classic cars are typically at least 15 years old, though some insurers view them as 25 years or older. Think 1960s Mustangs or early BMW 3-Series models.

- Vintage cars refer to vehicles that are generally older than 40 years, often pre-World War II models like the Ford Model T or the Rolls-Royce Phantom. Vintage vehicles were usually built from 1919 to 1930 (or 1940 for some insurers). These cars are especially rare and can carry hefty price tags at auctions.

- Modern classics are a newer category that includes relatively young but collectible cars like a 1990s Toyota Supra. These vehicles are older than 10 years and are of limited build.

There may be some overlap in age but think of it this way: All vintage cars are classic, but not all classics are considered vintage. The important thing to remember is that your car must meet your insurance provider’s specific definition of ‘classic’ or ‘vintage’ to qualify for a policy that suits your precious gem.

How are classic and vintage cars different from standard cars?

Except for the obvious differences in age, classic and vintage cars differ from standard ones in the following ways:

- Value: Unlike your everyday car that starts to depreciate the moment it leaves the dealership, classic and vintage cars age like fine wine. They can actually increase in value as time goes on.

- Repairs and parts: Finding parts for these old beauties can be like looking for a needle in a haystack. Plus, they often need a specialist mechanic. Both can make repairs and restoration costs skyrocket.

- Usage: You’re not driving these legends to the shops every day. Classic and vintage cars are generally only taken out of the garage for Sunday car meets or the odd special occasion. How often you use the car is one of the things insurers will look into when calculating your premium.

Why do I need specialised cover with classic and vintage cars?

Standard car insurance is designed for everyday vehicles – not rare collectibles. Here’s why your classic or vintage car requires something a little bit more bespoke:

- Agreed value coverage: Unlike standard policies that insure cars based on depreciating market value, classic car insurance lets you and your insurer agree on the vehicle’s value that accounts for on-road costs, modifications, options, or accessories found in the car.

- Limited use stipulations: Many classic car policies are tailored for cars that aren’t daily drivers but instead are used occasionally for shows, parades, or leisure rides.

- Special considerations: From covering restoration costs to ensuring access to specialist repairers, these policies consider expenses that would fall outside standard coverage.

What are the risks that classic car owners typically face?

Owning a classic or vintage car is a dream, but it’s not without its hiccups. Here’s what to watch out for when driving a head-turner:

- High theft risk: A flashy, classic car can easily catch the eye of thieves. With car thefts and burglaries from cars reaching a record high in the country (most of them happening right at your doorstep),1Car Expert – Car thefts reach record high in Australian state,2Australian Bureau of Statistics – Majority of car thefts happen at home having a rare beauty at home can easily keep you on edge.

- Costly restoration: As mentioned, repairs often involve rare parts and specialised mechanics – and they don’t come cheap.

- Susceptibility to damage: Your vintage car doesn’t have the safety standards that modern cars do, so it can be more prone to damage – and costly repairs.

What are the types of classic and vintage car insurance?

Typically, standard insurers offer several coverage options, each suited to protecting a different aspect of your prized possession.

Keep in mind that many specialist insurers generally offer comprehensive coverage for classic or vintage cars. Fair enough, as a lower level of protection like third-party property damage probably isn’t suitable for cherished classics!

Compulsory third-party insurance

Also known as a Green Slip if you’re in New South Wales, compulsory third-party insurance or CTP is a legal must-have for any car on Aussie roads. While it won’t pay for damage to your car or someone else’s property, it’s there to compensate for injuries or fatalities caused to others in an accident. This is the absolute *bare minimum* insurance everyday cars will need to stay on the right side of the law.

Third-party property insurance

Third-party property insurance has your back if your car accidentally damages someone else’s stuff – like their ride, their front fence, or even their house. It’s a budget-friendly option for those who don’t need full coverage but still want some peace of mind. However, most insurers of vintage or classic vehicles will only offer comprehensive coverage.

Third-party property, fire, and theft

Looking for something in between? This mid-level cover might hit the sweet spot. It includes the basics of third-party property insurance but adds extra protection against theft and fire. It doesn’t go quite as far as comprehensive coverage, but it’s ideal for owners who want decent protection for big risks without shelling out for premium-level insurance.

Comprehensive coverage

This is the gold standard for classic and vintage car lovers (and what most insurers of these vehicles often offer). Comprehensive car insurance takes care of damage to your car and other people’s property – whether you caused the bingle or not. Plus, it’s a lifesaver when it comes to risks like fire, storms, vandalism, or even theft (a real worry for these head-turners).

Helpful tip

Helpful tip

If you own a vintage or classic car, don’t skimp by going for a basic policy!

Here’s the thing: owning a classic or vintage car is a whole different ball game compared to your average runabout. These beauties aren’t just vehicles; they’re investments, memories, and sometimes even family heirlooms. That’s why going for a basic policy is a bit like using a flimsy umbrella in a downpour – it just won’t cut it when things get serious.

Comprehensive cover offers full protection and often comes with extras tailored for collectors. Things like agreed value payouts (so you don’t get short-changed on your car’s worth) and coverage that includes restoration costs or spare parts.

For someone who’s poured their heart and soul into their vintage or classic car, a comprehensive cover is worth its weight in gold.

Adrian Bennett

General Manager for General Insurance

How much does classic car insurance cost?

Here’s the million-dollar question: how much will it cost to insure your classic or vintage car? Just due to rarity and legacy alone, the cost for classic car insurancecan set you back more than a standard one. Still, the price will depend on a few factors:

- Age and model: Older, rarer vehicles cost more to insure.

- Condition: Is your Mustang showroom perfect or an ongoing restoration project?

- Usage: Limited usage and mileage typically reduces premiums.

- Agreed value vs. market value: Most classic car policies use agreed value because market value doesn’t reflect a collectible car’s true worth. For instance, some insurers in Australia often set premiums for historic car insurance based on agreed value.

How can I find a classic or vintage car insurance policy?

With so many options on the market, here are things to consider helping you choose the right policy for your cherished vehicle.

Specialist insurers provide tailored policies reflecting the nuanced needs of classic car owners. Standard car insurers might not offer the bells and whistles you need.

Look out for certain policy features that can meet the bespoke needs of your vehicle.

- Limited usage cover: Why pay the same as someone who’s driving their car every single day? If your car only gets out for the odd weekend cruise or special event, your premium can reflect how little you use it – fair’s fair, right?

- Lifetime guarantee on repairs: Some insurers provide a guarantee for any authorised workmanship and materials for as long as you own the car. Lifetime cover for all approved repairs, no ifs or buts.

- No blame, no penalty: Had an accident that wasn’t your fault? Some insurers allow you to waive the excess. Fair enough – why should you cop the cost for someone else’s mistake?

- Laid up cover: Got your hands dirty restoring your beloved possession? If your car’s not being driven during the restoration process, you might be able to trim down your premium while it’s laid up in the shed.

- Additional perks: Some insurers offer valuable benefits like emergency accommodation, trailer cover, or theft of keys and recoding.

Frequently asked questions

What are salvage rights?

If a collectible car is written off and it meets the insurer’s vehicle age requirement, salvage rights allow you to retain ownership of the wrecked vehicle for parts or restoration while receiving the payout worth of the car’s agreed value.

How should I register a classic or vintage car?

Registering classic and vintage cars varies for each state. For instance, Queenslanders need to complete the special interest vehicle registration concession application and satisfy the conditions for eligibility.3Queensland Government – Special Interest Vehicle Concession Scheme guide In NSW, classic car owners must complete conditional registration, which grants limited road access. The vehicle must either qualify as a historic vehicle or meet the eligibility criteria for classic vehicles.4NSW Government – Apply for conditional vehicle registration

How can I determine my car’s value?

Use a professional appraisal service or check recent auction results for similar vehicles. Keep any restoration and modification receipts and documents as these can also impact the car’s value.

Get started on comparing car insurance policies!

Save time and effort by comparing a range of car insurance quotes with iSelect

iSelect General Pty Ltd (ABN 90 131 798 126. AFSL 334115) has partnered with Compare the Market (ABN 83 117 323 378. AFSL 422926) to compare a range of car insurers and policies. Not all providers in the market or all policies offered by the partners are compared and not all policies or special offers are available to all customers.

A number of our participating general insurance brands are arranged by Auto & General Services Pty Ltd ACN 003 617 909 on behalf of Auto & General Insurance Company Limited 111 586 353, both of which are related entities of iSelect Limited. Our relationship with those companies does not impact the integrity of our comparison service. Click here to view iSelect’s range of providers.

Any advice provided by iSelect is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policy. You should consider iSelect’s Financial Services Guide which provides information about our services and your rights as a client of iSelect. iSelect receives commission for each policy sold that is a percentage of the premium or a flat fee. Ask us for more details before we provide you with any services.