.svg)

Public Liability Insurance

Public Liability Insurance

Written by

Gemma Kaczerepa

Edited by

David Rayfield

Reviewed by

Sharon KennyWhat is public liability insurance?

Public liability insurance is designed to provide protection for you and your business in the event a customer, supplier, or a member of the public is injured or sustains property damage as a result of your negligent business activities. It typically covers you for incidents that happen on the job, either at your premises or if you’re working on other job sites.

Who can bring a public liability claim?

Any third party who suffers an injury or property damage due to your business activities can file a claim. A third party is basically anyone who isn’t an employee – think customers, visitors, suppliers, or even members of the public.

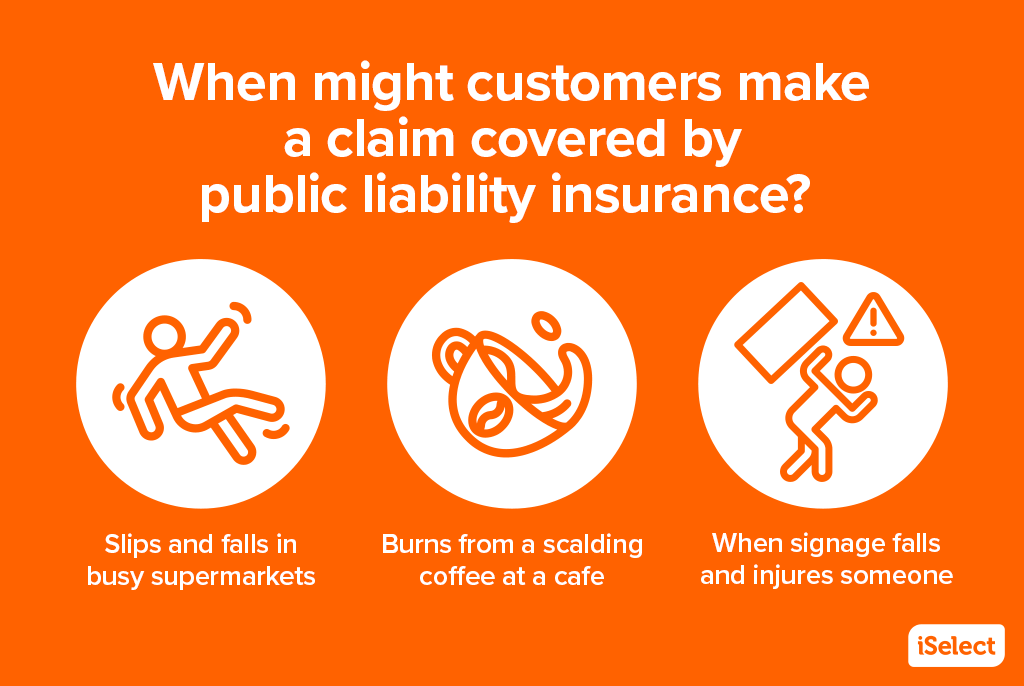

What could a public liability claim look like?

What does public liability insurance typically cover?

Medical expenses

If a third party is injured on your premises, such as a customer tripping on a loose mat and breaking their back, public liability insurance could cover their hospital bills, rehabilitation and medications, and even lost income if they can’t work.

Legal costs

If the matter ends up in court, public liability insurance may potentially save you thousands. It could help cover the costs of legal proceedings – like your defence costs, court expenses and settlement.

Property repair or replacement

Public liability insurance could potentially pay for repairs to a third party’s damaged property or even a full replacement if it’s lost or can’t be fixed. An example would be if you dropped a heavy tool and it landed on your client’s laptop, breaking it in the process.

Compensation for emotional distress

Public liability insurance isn’t strictly limited to physical injuries. If someone suffers emotional distress as a result of the incident, public liability insurance could potentially provide compensation.

Public liability insurance explained, with iSelect.

Learn more about public liability insurance, including what it covers, who it covers and some of the features to look for when choosing a policy.

How much does public liability insurance cost?

No two businesses are the same, which is why no two businesses will pay the same amount for public liability insurance. When calculating your premiums, insurance providers generally take into account different factors, such as:

- Coverage amount. It probably goes without saying that the more coverage you go for, the more you’ll likely have to pay for it

- Business size. Bigger businesses with more employees and higher revenue usually pay more for insurance because they’ve got greater exposure to potential claims

- Type of business. Different businesses face different risks, and some industries are inherently riskier than others – like construction versus consulting

- Location. Where you operate affects your price, because your location may be more prone to insurable events like natural disasters, theft or vandalism

Your public liability insurance questions, answered

What won’t public liability insurance cover?

Just like other types of insurance, public liability cover comes with a few exclusions. Here are some of the most common:

- Damage to your or your business’s property

- Injuries suffered by you

- Employee injuries or property damage (the former is covered by Workers’ Compensation)

- Intentional damage or injury

- Criminal acts

- Punitive damages (i.e. legal penalties), taxes or fines

- Incidents involving asbestos or pollution (these typically require separate cover)

What is and isn’t covered can also vary between policies. Make sure to check your product disclosure statement (PDS) for specifics related to your insurance

Will public liability insurance cover my employees?

Public liability insurance generally covers any damage or injuries caused by your employees while they’re on the job. But it doesn’t extend to injuries they suffer themselves.

Instead, this falls under workers’ compensation – a type of insurance that covers your employees if they get injured or sick at work. It’s mandatory for any business that has employees, no matter where you operate in Australia.*

Different types of employees may or may not be covered by workers’ comp. If you have apprentices, for example, they’ll be included in your workers’ compensation policy, but other workers such as independent contractors and unpaid interns might not. Check with your local state body to make sure.

*Please note BizCover does not offer Workers Compensation insurance.

Is public liability insurance mandatory?

This depends on the kind of business you run and where you operate. For example, all plumbers operating in Victoria need public liability insurance, as do electricians in Victoria, Queensland and Tasmania.

If you’re working on a public-facing job site, such as a building site or shopping centre, you might also require public liability insurance before you can start work – usually, this will be outlined in your job contract. Some businesses also need to take out public liability insurance before they can sign a lease on their premises.

For more info on the public liability insurance requirements in your state, check out our dedicated page:

How do I make a claim for public liability insurance?

The process can differ between insurers however it generally looks like this:

| Notify your insurer ASAP after the incident | |

| Fill out a claim form with a comprehensive rundown of the incident and any details about the third party’s allegations against your business | |

| Provide supporting documentation such as photos, videos, written correspondence, contracts between you and the third party, and any other relevant info | |

| Wait for your insurer to assess your claim |

What kinds of businesses might need public liability insurance?

Different kinds of businesses could take advantage of public liability insurance, especially those that work on external job sites or have members of the public visiting their premises. Even business owners who work from home may benefit from public liability insurance. If they’ve got clients or suppliers visiting their home office and something happens, it could provide valuable financial protection.

Some of the businesses that may want to consider public liability insurance include:

- Retail stores

- Restaurants and cafes

- Construction companies

- Tradespeople (such as electricians and plumbers)

- Event organisers

- Freelancers and consultants who work on job sites

- Beauty salons and spas

- Fitness instructors and gyms

- Medical clinics

- Photographers and videographers

- Real estate agencies

- Childcare centres

- Catering businesses

- Market stall operators

- Manufacturers

- Cleaning companies

- Landscapers and gardeners

- Health and wellness practitioners

- Venues and rental spaces

- Tour operators

What’s the difference between public liability and professional indemnity?

Public liability and professional indemnity insurance are often confused – and rightly so! Each one is designed to protect you from risks involving third parties. But there are a few differences between the two.

Public liability insurance could protect you financially if a third party is injured or something happens to their property and your business is responsible – such as a slip and fall on your premises or a broken window.

On the other hand, professional indemnity insurance may offer financial protection if a third party suffers financial losses due to negligence or errors arising from your professional services or advice. A good example would be if you recommended a client install a particular software system and it resulted in a data breach.

It’s a common type of insurance among financial advisers, management consultants, accountants, lawyers and health professionals.

iSelect and BizCover have teamed up to make finding business insurance easier. Using our comparison tool, you can easily weigh up policies from a range of insurers. Get started online today.

This information is general only and does not take into account your objectives, financial situation or needs. It should not be relied upon as advice. As with any insurance, cover will be subject to the terms, conditions and exclusions contained in the policy wording.

© 2025 BizCover Pty Limited, all rights reserved. ABN 68 127 707 975; AFSL 501769

Get started on comparing business insurance today!

We’ve partnered with BizCover to help you compare from a range of business insurance policies.

iSelect’s partnered with BizCover Pty Ltd (ABN 68 127 707 975: AFSL No.501769) to help you compare small business insurance policies. iSelect earns a commission from BizCover for every policy sold through the website or contact centre. iSelect and BizCover do not compare all providers in the market, or all policies offered by all providers. iSelect does not arrange policies from the providers we compare for you directly, but iSelect will refer you to our trusted partner, BizCover Pty Ltd who can.

Any advice provided on this website is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policy. You need to consider if the insurance policy is suitable for you. Please read the Financial Services Guide before buying any insurance policy.