.svg)

Handyman Insurance

Handyman Insurance

Written by

Gemma Kaczerepa

Edited by

Ellie Garran

Reviewed by

Sharon KennyCompare business insurance the easy way

We’ve partnered with BizCover to help you compare business insurance policies.

Why might handymen need business insurance?

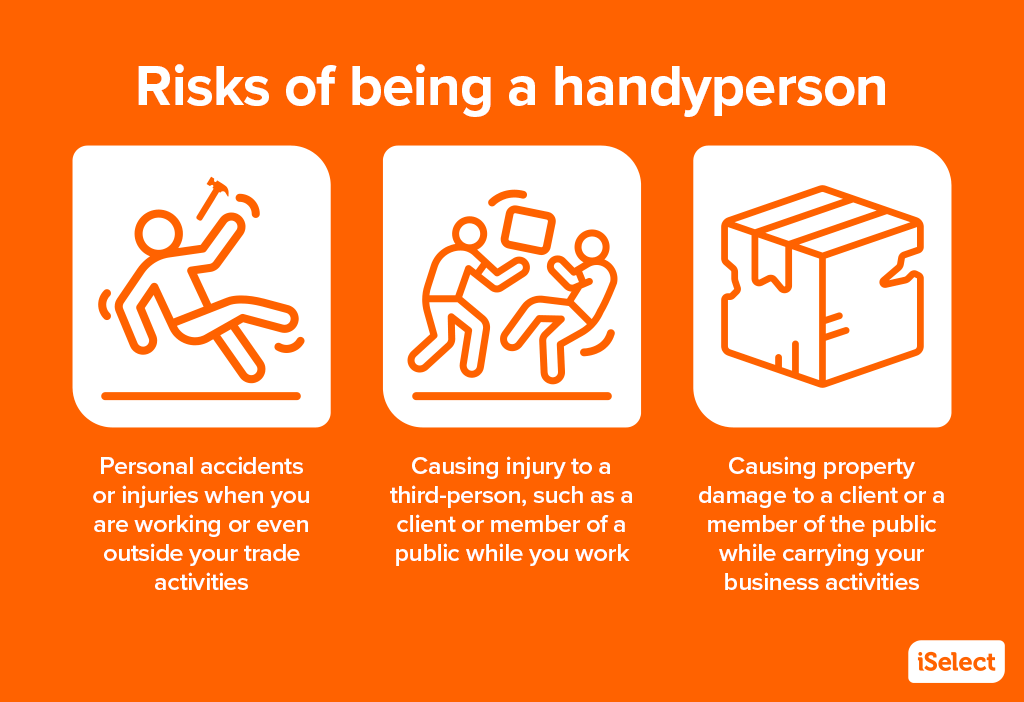

A job as diverse as being a handyman comes with several equally diverse challenges. From falling off your ladder or having your tools stolen off the back of your ute, each and every day you run into some kind of hurdle.

While business insurance probably won’t shield you from your client’s questionable preferences, it can help cover some unexpected costs – such as lost income if you’re recovering from that ladder fall, repairing damages caused by your business activities or replacing your stolen tools – just to name a few. It acts as a financial safety net if something goes wrong, and it could potentially mean avoiding spending thousands of dollars on legal costs, damages and other unforeseen expenses.

Business insurance may be especially handy if you’re a sole trader. This is because sole traders are personally liable for any business-related debts and legal claims, and insurance may help you avoid the risk of losing personal assets like your home, ute or truck, and savings.

What are some risks associated with being a handyperson?

What kind of cover might be relevant for handypersons?

There’s no single business insurance product for handypersons, but there are several types of insurance that may be relevant to you.

Public liability insurance

As a handyman and handywoman, you’re likely working on all kinds of public-facing job sites, be it a client’s home or an office building. Naturally, interacting with members of the public exposes you to different risks, like accidental property damage or injuring someone on-site.

Public liability insurance is designed to mitigate the financial fallout from those risks. It covers third-party property damage and injury that your handyperson business is responsible for, and includes costs such as medical expenses, replacing or repairing someone’s property, and legal fees.

Portable equipment insurance

Without valuable items like your toolbox and power tools, you probably wouldn’t be able to get much done. This is why portable equipment insurance can be such a vital safety net – it could cover the cost of replacing your tools and equipment if something happens to them.

There are a few scenarios that portable equipment insurance can provide coverage for, including theft and accidental damage.

Personal accident and illness insurance

Handyperson work involves a lot of physical labour, so if you are a sole trader not covered by Workers Compensation, and you suddenly couldn’t climb up a ladder or lift heavy tools as a result of an injury or illness, how would you ensure your business could stay afloat?

Personal accident and illness insurance provides coverage if you get sick or injured on or off the job and can’t work for an extended period. It can cover up to 85% of your lost income until you’re back on your feet and back to climbing ladders again.

Helpful tip

It might be tempting to go for the cheapest policy, but if you need to make a claim, you might find you don’t have adequate coverage or end up paying a higher excess. It’s about balancing affordability and comprehensive coverage to find what suits you.

Is insurance mandatory for handywomen and handymen?

This really depends on the specifics of your job contracts, whether you have people working for you and the kind of work you do.

As far as contracts go, some stipulate that you must have a minimum amount of public liability insurance before undertaking a job. This is often a requirement of any job that’s exposed to members of the public, like a construction site. There may be other types of insurance required too, such as professional indemnity insurance.

If you’ve got employees, you’ll need to take out workers’ compensation, which is mandatory in every state and territory. It covers your employees if they get sick or injured on the job and is typically required for subcontractors and apprentices, too.* If you are a sole trader you may want to consider Personal Accident and Illness insurance to cover you for these type of risks – in and off work.

Lastly, while many handymen undertake jobs such as repairs, painting and carpentry, some may offer other services like plumbing and electrical work. Some states actually require these trades to have adequate insurance. In Victoria, for instance, plumbers must have a minimum amount of public liability insurance., Meanwhile electricians in Tasmania need public liability coverage, too.

*Please note BizCover currently does not offer Workers Compensation insurance.

How much does business insurance cost for handymen?

Different handymen typically pay different amounts for business insurance. This is because several factors go into determining the cost, and each is as personal as the next. The main ones include:

- The type of work you do. You might work mostly on residential jobs, or you may work on large-scale commercial projects including office buildings and retail spaces. Or, you could also offer services like carpentry, electrical, plumbing or painting. Your insurance provider will assess your level of risk and tweak your premiums accordingly. For instance, a handyman who does commercial work and the occasional plumbing repair may pay more than someone who focuses mostly on odd jobs in people’s homes.

- The size of your business. The bigger your business, the more risks you face. You might have multiple employees, and each one adds to the potential liability. You may bring in lots of revenue, which could mean you need more coverage.

- Your location. Each state and territory has its own rules around insurance requirements for certain trades. Plus, even the specific location where you work can impact cost. Insurance providers often look at the claims history in your area when assessing your premiums, considering crime rates and the incidence of natural disasters.

- Your claims history. On that note, your individual claims history is a major factor too. If you’ve made lots of claims in the past, your premiums may be higher.

- Policy specifics. Different policies have their own features, exclusions and coverage limits. You might also choose extras like specifically listing valuable power tools in your portable equipment insurance, which can jack up the price of your policy.

How can I assess how much business insurance I need?

There’s no one-size-fits-all insurance solution for handypeople, just like there’s no one-size-fits-all spanner. But the following steps can help you estimate your insurance needs:

- Identify potential risks. What are the risks inherent to your job? Are you a handyman who works with power tools and heavy machinery, or do you mostly focus on small repairs? If your handyman work comes with a lot of risks, you might need greater insurance coverage.

- Assess your business assets. Do a stock take of all your business assets, including your tools, ute or truck, workshop and that collection of spare parts you swear you’ll use someday. The more you have, the higher you may need to make your coverage limit to ensure everything’s protected.

- Review client and legal requirements. Some clients might specify the types of insurance you need before they work with you, such as public liability or professional indemnity insurance. There may also be legal requirements attached to your trade, particularly if you’re undertaking plumbing or electrical work.

- Determine coverage needs and limits. Based on the risks, assets and requirements you’ve identified, figure out which types of insurance and the amount of coverage you need. Make sure your coverage limits are high enough to adequately cover potential claims or losses.

Where can I find and compare business insurance?

Together with BizCover, we’ve launched a handy business insurance comparison tool to make comparing policies simple. You can use the tool to weigh up policies from several of Australia’s leading insurance providers.

This information is general only and does not take into account your objectives, financial situation or needs. It should not be relied upon as advice. As with any insurance, cover will be subject to the terms, conditions and exclusions contained in the policy wording.

© 2025 BizCover Pty Limited, all rights reserved. ABN 68 127 707 975; AFSL 501769

Get started on comparing business insurance today!

We’ve partnered with BizCover to help you compare from a range of business insurance policies.

^As with any insurance, cover is subject to the terms, conditions and exclusions contained in your policy document. The information contained on this webpage is general only and should not be relied upon as advice.

iSelect’s partnered with BizCover Pty Ltd (ABN 68 127 707 975: AFSL No.501769) to help you compare small business insurance policies. iSelect earns a commission from BizCover for every policy sold through the website or contact centre. iSelect and BizCover do not compare all providers in the market, or all policies offered by all providers. iSelect does not arrange policies from the providers we compare for you directly, but iSelect will refer you to our trusted partner, BizCover Pty Ltd who can.

Any advice provided on this website is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policy. You need to consider if the insurance policy is suitable for you. Please read the Financial Services Guide before buying any insurance policy.