.svg)

Life Insurance for Young Singles

Life Insurance for Young Singles

Written by

Madeline Pettet

Edited by

Laura Crowden

Reviewed by

Adrian BennettEasily compare life insurance quotes

Save time and effort by comparing life insurance with iSelect’s trusted partner Lifebroker

What is life insurance?

Long story short

Getting life insurance when you’re young may help support your financial security and independence later

It’s an unhelpful myth that you don’t always need it if you’re young and healthy.

Your life insurance premium could be comparatively cheaper now than when you’re older

It might be worthwhile looking at different premium structures over the long term.

You’re also more likely to be eligible for cover when you’re young and healthy than down the track

Even if your health worsens, you could keep the cover you took out when you were younger and healthier.

What is life insurance?

Life insurance is an umbrella term referring to a range of insurance products aimed at financially supporting you and your loved ones if something unexpected were to happen to you. This could include if you’re unable to work for a time due to serious illness or injury, you become totally and permanently disabled, or you pass away.

Do I need life insurance if I’m young and single?

It’s a bit of a myth that life insurance is only for when you’ve hit certain life milestones, like marriage, kids, and mortgages. However, like having a go-to dentist and GP, life insurance can be a pretty handy thing if you’re a young adult – even if you’re not planning on settling down any time soon.

Myth: I’m young and healthy, I don’t need life insurance

One of the great things about being young is that there’s so much potential ahead of you. No one knows what the future will hold, and this can be both exciting and a little overwhelming.

With this in mind, the sad reality that Millennials and Gen Z will likely have lower home ownership rates than previous generations emphasises the importance of protecting your earning power and savings, including your superannuation, from the get-go. Life insurance can be one way to help you stay financially resilient, even at a time when many young Aussies are feeling the pinch of the rising cost of living and growing more concerned about their overall financial security.

Whether it’s helping cover a portion of your income if you’re unable to work for a time due to a serious injury or illness, or paying a lump sum if you can’t ever work again due to an acquired disability, life insurance products might help you weather storms that may otherwise send your short and long-term plans overboard.

Myth: I don’t have any dependents, I don’t need life insurance

Even if you’re young, unattached, and childfree, you still have someone who relies on you: yourself! While so far you may have always been able to rely on yourself to get the bills paid and keep food on the table, what if something unexpected were to happen to you, like becoming seriously injured or ill? Life insurance products could help you remain as independent as possible by assisting with your day-to-day expenses or adapting your lifestyle to an unexpected change.

Additionally, it could mean you’re able to stay in your current home – even if you’re just renting – keeping those crucial social networks intact, while also keeping as much routine as possible in your life at a stressful time.

In Australia, we’re lucky to have social welfare support and injury and disability schemes. However, like hoping your parents, siblings, and friends have got your back, this support isn’t always an option for everyone or in every circumstance. Life insurance, though, could help fill the gap if you’re ineligible or unable to access these services and support.

Why should I consider life insurance when I’m young?

You might have lower premiums

To calculate life insurance premiums, insurers look at a range of risk factors. These include your age, health, and medical history. So, the younger and healthier you are when you first take out a policy, the lower your premium is likely to be.

You might have fewer issues now than down the track

Speaking of your health, if your medical history is particularly checkered, you may find it tricky to get the level and type of cover you’d like. However, opting for cover sooner – and when you have a shorter, less serious medical history – can ensure you have cover if your health worsens as you age. Life insurance policies are ‘guaranteed renewable’, meaning whatever you’re covered for at the start of your policy will be covered for as long as you hold the policy, no matter what the future holds. Assuming, of course, you keep paying your premiums!

You won’t be eating into your superannuation for retirement

A choice you make today might seriously change your future. You could skip life insurance altogether and hope you’re always able to work while enjoying a clean bill of health. Alternatively, you might opt for life insurance through your superannuation, but this can eat away at your overall superannuation balance, as well as increase the risk of being underinsured. Choosing direct life insurance – that’s life insurance bought directly from an insurer – could be a decision your future self is grateful for.

You can enjoy peace of mind

You likely already have plenty of worries keeping you awake at night, from pursuing your dream career path to planning out your next big holiday. Life insurance could give you invaluable peace of mind when it comes to your future. While you can’t control what happens to future you, you can at least be prepared for the worst and hope for the best.

What types of life insurance are best for young adults?

As is the case with most insurance, there’s no such thing as a ‘best’ life insurance for young adults. Life insurance isn’t ‘one-size-fits-all’ but rather it’s about picking a policy that works for you. However, people who are young, single, and currently have no dependents, may consider different types of life insurance which cover serious injury or illness. Again, this depends on your unique circumstances.

Income protection

Of the four main types of life insurance, income protection is commonly purchased by younger adults, but it can depend on the person’s circumstances. With an income protection policy, you could receive up to 70% of your monthly pre-tax income for a set benefit period if you’re unable to work due to an injury or illness. This ongoing monthly payment could help you stay on top of bills while you rest up and recover. Waiting periods might apply, however.

Some policies also come with additional cover benefits to help you on your road to recovery, like rehabilitation.

Total and permanent disability (TPD) insurance

TPD insurance provides a lump sum benefit if you become totally and permanently disabled, and are unable to work again as a result. These funds can help with medical costs, as well as help you adapt your life to a change of circumstances. For instance, the lump sum may help to cover modifying your home to allow you greater independence, where possible.

Something young singles may consider is that the prevalence of disability increases as we age. In fact, by age 65, half of Aussies have some form of disability, although these may not always be serious impairments to their daily life and meet TPD policy definitions.1Australian Institute of Health and Welfare – People with disability in Australia 2024, p31

Trauma insurance

Trauma insurance pays a lump sum benefit if you’re diagnosed with a specified illness or injury. While you may still be able to work, the payment can reduce your financial stress as you undergo treatment and recover. Trauma insurance might be able to help you afford to reduce your hours or even take some extended time off for treatment.

Prioritising your health isn’t anything new, but it may be becoming more important for younger Australians. For instance, cancer incidence in the younger population has risen significantly, compared to rates back in 2000. Those in their 30s were roughly 20% more likely to be diagnosed with at least one of a range of cancers, while the likelihood jumped up to about 43% for those in their 40s.2Australian Institute of Health and Welfare – Cancer data in Australia Similarly, mental illness prevalence is increasing more rapidly than many other serious illnesses, with women aged 15 to 34 most affected.3Australian Institute of Health and Welfare – Prevalence and impact of mental illness

Having trauma insurance may be part of your overall health and wellbeing strategy in case you ever need more than a gym membership and a plate full of vegetables.

Term life insurance

Term life insurance pays a lump sum to your chosen beneficiaries if you unfortunately pass away or are diagnosed with a terminal illness. While term life insurance is commonly a product many families take out to ensure any dependents have financial support if the worst happens, being young and single doesn’t necessarily rule you out.

For instance, term life insurance could enable you to help out your parents or a sibling in the future. You mightn’t be there to pick up their groceries or make a cuppa, but you could still help financially support them.

Additionally, if you have debt, such as a mortgage, car loans, or credit card debt, when you pass away, your loved ones may be left to cover what remains. If you held term life insurance, this might mean they have funds to clean the slate or at least make a little more progress towards it. The payout can also be used to cover your funeral expenses.

Helpful tip

Helpful tip

If you’ve written off life insurance as too expensive, it might be time to run the numbers again, including thinking about what peace of mind is worth to you. After all, life insurance is there to help make things a little easier when things feel like they couldn’t get any worse.

Don’t forget, too, your youth and (hopefully) healthy medical history could work in your favour for potentially lower premiums.

Adrian Bennett

General Manager for General Insurance

How much does life insurance cost for young adults?

Lots of factors affect how much life insurance premiums cost. Some of these include:

- your age

- your health and medical history

- your lifestyle choices, including smoking and risky hobbies

- your chosen level of cover.

That means as a younger person with hopefully fewer medical and health risks, you’ll likely enjoy lower life insurance premiums.

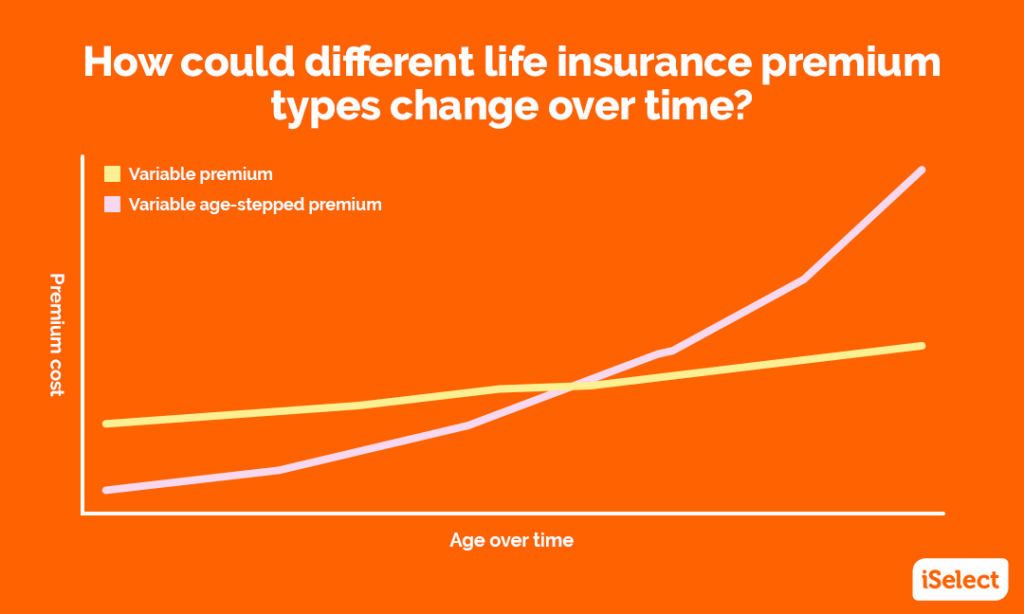

Additionally, life insurance policies generally come with two premium options: variable and variable age stepped. Variable premiums are calculated using the age you were when your cover started, averaging out over a number of years. Meanwhile, variable age-stepped premiums are recalculated using your age at each policy anniversary.

If you’re intending to keep your life insurance for a long time, the premium type you choose could make a difference. For instance, if you’re starting a policy young, you may find a variable premium ends up with fewer increases over time compared to a similar variable age-stepped premium. As a result, it might mean comparatively cheaper cover as you get older.

FYI: whichever premium type you pick, the price may change due to factors beyond your age.

Note: This graph is for illustrative purposes only and your premium comparison may be different. The graph assumes indexation is applied to cover automatically to ensure it keeps pace with inflation. No other kinds of changes to premiums are shown.

How much life insurance do young singles need?

The answer is in the question for this one: it’s all about need, both now and in the future. You might like to try assessing your needs – in this case, your financial obligations. Do you have any debts and ongoing expenses? And, even if you can’t tell the top of a crystal ball from its bottom, you may want to consider how those financial obligations could change as you hit your strides in life.

You could then weigh this assessment up against the different policy types. For instance, could income protection offer the kind of cover you’re after?

But it’s worth keeping in mind that you can always adjust your cover down the track as you age or your needs change.

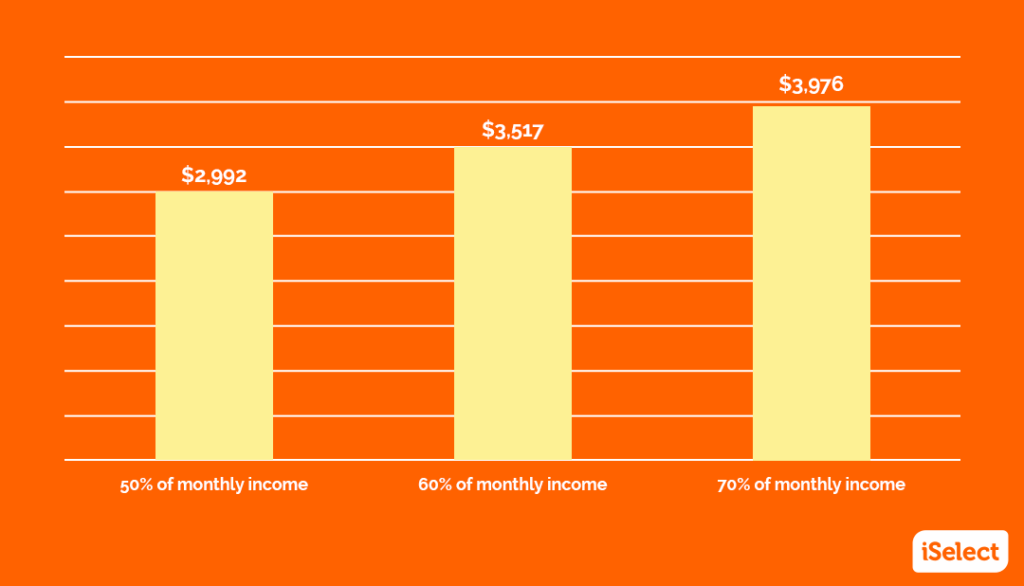

How much life insurance cover should Tom choose?

Our fictional friend Tom works at an independent video game company, helping to plan out divergent storylines. He’s paid $6,547 monthly, but that’s before any tax or super contributions.

He does his best to save $100 a week from his pay, spending the rest on rent, food, clothing, transport, and catching up with his friends out and about in the city. He estimates he spends $3,380 each month on essentials.

Most insurers offer cover up to 70% of your income but Tom isn’t sure he needs that much so looks at an income protection policy that offers three benefit options: 50%, 60%, or 70% of his monthly pre-tax income. Each benefit option comes with a 30 day waiting period and a two-year benefit period.

To help Tom decide which cover option he prefers, he calculates each percentage of his income and what he’d roughly pay in income tax on any benefits, assuming those benefits were the only income he received in a financial year.

Note: Example is hypothetical. Your scenario may be different. Only whole numbers used in calculations. FY24–25 income tax rate applied; does not include Medicare levy. Tom does not have any tax rebates or offsets.

Crunching the numbers, Tom realises he might struggle with only 50% of his income coming in. It could mean making some changes to his budget, along with dipping into his savings or relying on help from friends and family.

While he likes the idea of having more cash to splash with 70% of his monthly income, he’s not sure if he’ll really needs that much. He thinks he’d prefer to go for 60% and hopefully have a lower monthly premium as a result.

Where can I find and compare life insurance?

Life insurance might not be the sexiest topic, but, like the birds and the bees, it’s something we should all be across by the time we’re young adults. Thankfully, iSelect’s online comparison tool helps make it easy to weigh up policy quotes from a range of insurers. Try it today to see how you can help protect your future.

Easily compare life insurance quotes

Save time and effort by comparing life insurance from a range of policies and providers with iSelect’s trusted partner Lifebroker

iSelect’s partnered with Lifebroker (AFS Licence number: 400209) to help you compare a range of Life Insurance policies. iSelect earns a commission from Lifebroker for each customer referred through the website or contact centre. Lifebroker do not compare all life insurers or policies in the market.

iSelect Life Pty Ltd – ABN 89 124 304 347, AFS Licence Number 331128. Any advice provided by iSelect is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policies. You should consider iSelect’s Financial Services Guide which provides information about iSelect services and your rights as a client of iSelect.’