.svg)

What is Rentvesting and How Can It Help Me Afford a Property?

What is Rentvesting and How Can It Help Me Afford a Property?

Written by

Liv Steigrad

Edited by

Ellie Garran

Reviewed by

Sam HymanCompare home loans the easy way

We partnered with Aussie to help you compare home loans from over 25 lenders and over 2,500 home loan products.

Rentvesting is the strategy of renting a place to live while investing in property elsewhere.

If you mention you’re rentvesting in the group chat and your mate asks, ‘Is this another one of your made-up throwaway lines?’ you can tell them this:

Rentvesting is a combo of renting and investing, and it’s a trend making the rounds in Australian real estate—thank you very much.

Put another way, it means you:

- buy a property you can afford

- rent it out

- rent a property somewhere else to live in.

In recent years, Australia’s housing market has seen sky-high property prices. It often puts home ownership out of reach and puts off many young Aussies from buying properties.

This is likely one of the reasons why rentvesting has become an appealing way to enter the property market and build wealth.

How does rentvesting work?

Imagine living in your dream city apartment with all its perks, while your investment property somewhere affordable is working hard to build your wealth.

It’s equal parts savvy and cheeky, really.

You get the best of both worlds—enjoy the lifestyle and location you like while kicking some major investment goals.

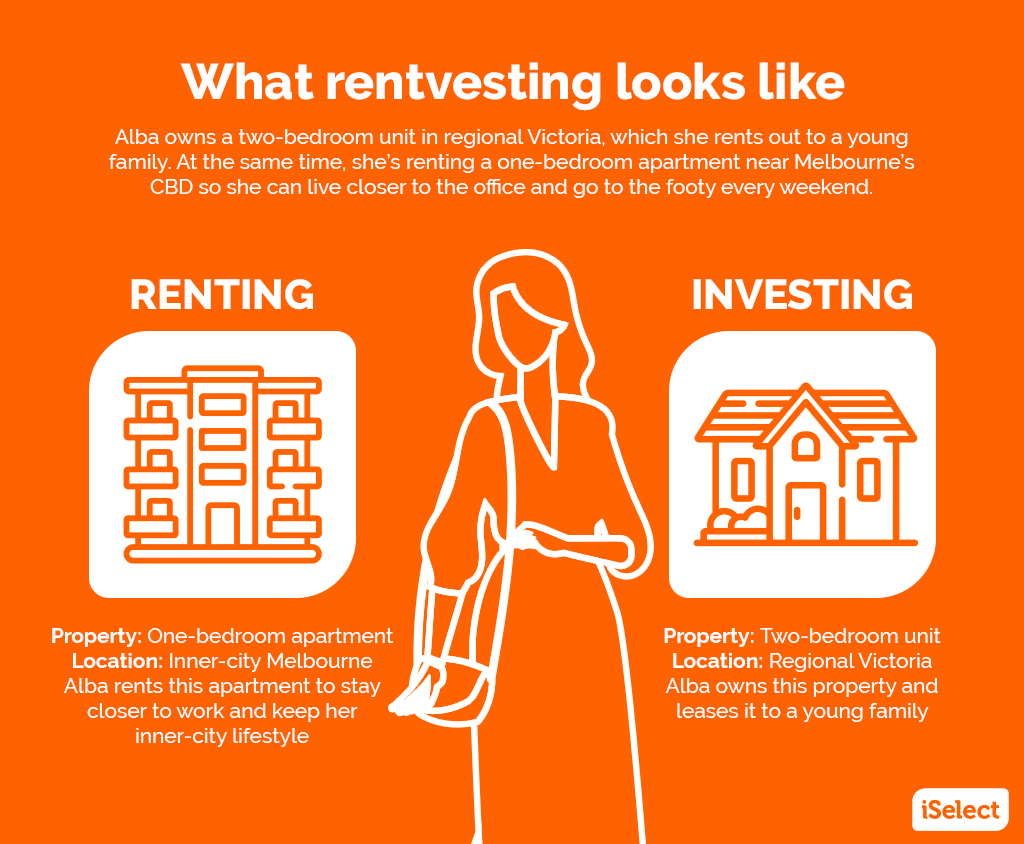

Take our fictional savvy heroine Alba, for example. She’s a 30-something professional living in Richmond, near Melbourne’s CBD. She’s practically married to her job and has saved enough downpayment for her first property.

But Alba isn’t too keen on the astronomical costs of buying property anywhere near Melbourne, one of Australia’s more expensive cities. Instead of forgoing her inner-city lifestyle or stretching her finances to breaking point, Alba opted for rentvesting.

Alba bought her first property in the regional city of Warrnambool—a two-bedroom unit with a decent backyard—which she’s currently renting out. It’s cheaper than most of what she could find in Richmond.

While her rental property in Warrnambool is almost paying for itself, Alba gets to enjoy walking to the MCG to watch the Pies, go for a back-to-back and indulge her late-night pho cravings along Victoria Street.

What are the benefits of rentvesting?

One lovely Saturday arvo at her sister’s birthday, Alba’s nan asks why she’s still renting when she already owns a property.

So here’s what Alba’s put together on her Notes app for the next time she’s asked:

Maintaining your lifestyle

Rentvesting meets you where you’re currently at in life. It allows you to get into the property market without sacrificing the lifestyle you want.

Young professionals like Alba who want to live closer to the city or families who need more space might not be able to afford a home that suits them. With rentvesting, they can still get into the property market by buying something smaller or further out.

Renting is cheaper than buying a property in the vast majority of Australian suburbs. This is likely one of the reasons rentvesting is becoming more popular in Australia.

Freedom to live anywhere you like

Rentvesting means you’re not tied to living in one particular place. You have the freedom to move houses with less admin and number-crunching.

If you decide to rent in an inner suburb but then find it’s not your vibe, it’s easier to find a house for lease elsewhere than to sell your own property.

You can also live in a rental property where amenities and services are within reach. You can take a few flights of stairs for the gym in an apartment, have more childcare options closer to work, or let your choco labrador live its best life with a big backyard and a footy oval across the road.

Potential tax benefits

Owning an investment property can come with tax benefits, too.

Homeownership can come with a whole lot of extra expenses: interest on your loan, council and strata fees, land tax, maintenance and repairs. The list goes on.

When that property is an investment rather than a home, you can claim these expenses as tax deductions.

If you have the cash flow to support it, negative gearing (when your costs are greater than your rental income) means any financial losses can be deducted against your other streams of income like your salary or other investments. In other words, you get to reduce your overall taxable income.

In Alba’s case, while her rental property is almost paying for itself, all the costs associated with repairs and maintenance in her Warrnambool property can add up. She can tap into negative gearing and reduce her overall taxable income, potentially getting tax benefits.

Consider consulting a financial advisor or accountant to understand how rentvesting could impact your tax situation.

Greater financial flexibility

Say Alba looked at her budget and realised she could afford $4,000 a month on housing.

Her inner-city rental costs $2,400 a month. Her regional property has a monthly mortgage of $3,000, which is covered by its rental income.

That leaves her with $1,600 a month that she can put to use to continue to grow wealth. She’s deciding between these options:

- make extra repayments towards the mortgage to pay it off faster

- put it in an offset account or redraw facility to reduce her payments and improve her cashflow

- put it aside to save up for her long-term dream home

- invest it in an exchange-traded fund.

Getting into the property market sooner

Think about your long-term dream home.

What features does it have? Where is it? Can you afford it now?

Rentvesting allows you to buy a cheaper home, which means you can get into the property market earlier. The earlier you get into the property market, the more time you have for the properties to grow in value and provide rental income, helping you build your wealth faster and maybe even helping you buy your dream home sooner.

Helpful tip

Helpful tip

Thinking about rentvesting? Make sure you’re buying for the renter, not just the location.

Post-pandemic, it’s less about city views and more about space to breathe; think home offices, backyards, and lifestyle perks. Check out vacancy rates and see what’s in demand in the area. Smart rentvestors don’t just buy well; they buy wisely.

Sam Hyman

General Manager – National Sales, Aussie

What are the drawbacks of rentvesting?

While many people think of property as a relatively safe investment strategy, rentvesting comes with some degree of risk—just like any other investment.

Here are some of the pitfalls to watch out for.

Higher interest rates

Investment properties tend to come with higher interest rates than owner-occupied Home Loans.

Relying on rental income

If the rental income covers all or most of your mortgage payments, congratulations. You struck gold!

But what if you can’t find a tenant for a while? Can you cop some of the mortgage payments while looking for people to rent your place? How long can you do this?

Missing out on first home benefits

Buying an investment property as your first property means you miss out on the First Home Owner Grant and its benefits, which can add up to thousands of dollars.

Capital gains tax

If you sell an investment property for more than you bought it for, you’ll have to pay capital gains tax on your profit. If you sell a property that you were living in, you don’t get charged capital gains tax.

Relying on the rental market

Rentvesting comes with a degree of reliance on the rental market. The rent you can charge depends on the supply and demand of similar properties.

If demand for properties like yours is high (and supply is low), you’ll be able to charge higher rent and be more picky about your tenants.

On the other hand, if it’s a ‘renters’ market’ (supply is high and demand is low), you may have fewer tenants to choose from and have periods without tenants.

| Pros and cons of rentvesting | |

| Maintaining your lifestyle | Higher interest rates |

| Freedom to live anywhere you like | Capital gains tax |

| Potential tax benefits | Missing out on first home benefits |

| Greater financial flexibility | Relying on rental income |

| Getting into the property market sooner | |

What are some alternatives to rentvesting?

Of course, rentvesting isn’t the only way to get into the property market.

Buying to live

If you can afford a place you’d like to live, buy-to-live loans often come with lower interest rates.

Buying to sell

Buying to sell, also known as property flipping, is when you buy a property, make some improvements, then sell it for a profit relatively quickly.

While this can seem like a quick way to make a profit, you do need considerable cash to cover the purchase costs, renovation or improvement costs, and loan repayments in the meantime.

Remember that you might not be able to rent the property out while it’s being fixed up.

Property schemes

A property scheme essentially involves pooling your money with other investors and putting it into property assets. An investment manager buys and manages investment properties on your behalf.

Property schemes can give you access to more types of investments, including construction, industrial, and commercial real estate. Depending on the type of property scheme, you might get quarterly or half yearly income.

Where can I find and compare Home Loans?

We’ve teamed up with Aussie to simplify the process of finding a suitable Home Loan. Get started comparing from a range of lenders online.

Get started on comparing home loans today!

Find a home loan by comparing with iSelect’s trusted partner, Aussie.

iSelect is the trading name of iSelect Mortgages Pty Ltd (ABN 86 148 217 181). iSelect Mortgages Pty Ltd is a credit representative (Credit Representative 400540) of Lendi Group Distribution Pty Ltd (Australian Credit Licence 246786). iSelect provides a referral to Lendi Group Pty Ltd, a Credit Representative of Lendi Group Distribution Pty Ltd (Australian Credit License 246786). iSelect Mortgages Pty Ltd receives a commission from Lendi Group Distribution Pty Ltd, the licensee for each new customer account created and for each home loan submitted through this service.