.svg)

What Is Mortgage Stress?

What Is Mortgage Stress?

Written by

Tina Sendin

Edited by

Ellie Garran

Reviewed by

Sam HymanCompare home loans the easy way

We partnered with Aussie to help you compare home loans from over 25 lenders and over 2,500 home loan products.

Mortgage stress is the financial difficulty of keeping up with home loan repayments. While you probably know whether you’re stressed or not, the term is commonly used when someone’s mortgage makes up more than 30% of their household income. (There’s no hard and fast rule on this percentage, but 30% seems to be the consensus among major banks and lenders in the country).

What causes mortgage stress?

With mortgage stress, you’re likely to experience the pressure of keeping your head above water because of economic reasons: job loss, reduced income, rising cost of living, or fluctuating interest rates.

Mortgage stress can also be caused by a significant change in life circumstances, such as starting a family, facing an illness, losing a loved one, or separating from a partner.

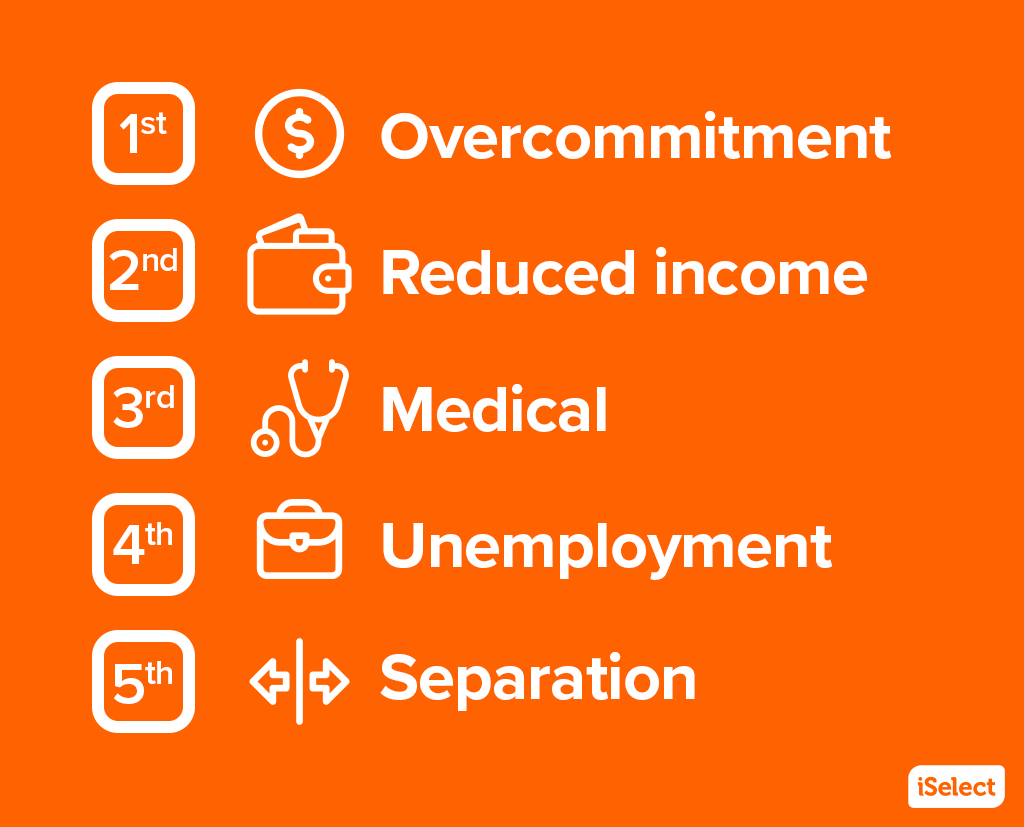

What’s interesting, though, is that, according to a survey rolled out by the Australian Securities and Investments Commission, the most common reason why Australians are seeking mortgage-related hardship assistance is overcommitment.

Here are the most common reasons they found people sought help for mortgage stress:

Source: Australian Securities and Investments Commission – Hardship, hard to get help: Lenders fall short in financial hardship support, p6

This might be related to what’s called a mortgage cliff.

Remember during the pandemic, when many Aussies took advantage of the extremely low interest rates of 2%? Most of those who went on fixed rates are seeing their loans rolling over to variable rates, which is about triple the value of their previous ones. It’s as if they were taking a gentle walk and then a cliff suddenly appeared in front of them – not ideal!

Some of these homeowners – like, 5.8 million of them – have struggled to make repayments over the last year.

How common is mortgage stress in Australia?

According to the International Monetary Fund (IMF), Australia has the highest level of mortgage stress in the developed world.

The good news is mortgage stress is starting to go down since its alarming highs in early 2024.

The not-so-good news? The number of Aussie homeowners ‘extremely at risk’ of mortgage stress still amounts to 994,000, or 20% of mortgage holders – two years after interest rates started to rise in May 2022.

If you add the surge in mortgage hardship claims and home resales (16% of which are for properties purchased from less than three years ago), we’re looking at a grim homeownership situation in the country today.

All these sobering statistics mean one thing: If you’re feeling under the mortgage pump, you’re not alone.

‘Mortgage stress is real. My partner and I are currently paying two mortgages and it feels overwhelming thinking about how we can stay on top of our monthly repayments alongside the rising cost of living. Selling the other property to free up our cashflow is always at the back of our heads. We’re doing everything to cut down on expenses, but if interest rates go any higher, we might have to seriously consider other financial strategies!’

Tina Sendin

Digital Writer, iSelect

What is the Australian Government doing to address mortgage stress?

The Australian Government has put certain affordable housing measures in place to address stress in Aussie households, not just in paying mortgages but also ensuring everyone gets a roof over their heads. They include the following:

Cost-of-living tax cuts

Impacting 13.6 million Australians, the tax cuts introduced on 1 July 2024 aim to help ease the rising cost of living. The changes mean that:

- people with lower incomes are taxed at lower rates

- the income thresholds to be taxed at higher rates have increased.

The changes look like this:

| 2023–24 | 2024–25 | ||

| Thresholds ($) | Tax rates (%) | Thresholds ($) | Tax rates (%) |

| 0 – 18,200 | 0 | 0 – 18,200 | 0 |

| 18,201 – 45,000 | 19 | 18,201 – 45,000 | 16 |

| 45,001 – 120,000 | 32.5 | 45,001 – 135,000 | 30 |

| 120,001 – 180,000 | 37 | 135,001 – 190,000 | 37 |

| Over 180,000 | 45 | Over 190,000 | 45 |

Source: The Treasury – Tax cuts to help with the cost of living

These tax cuts could benefit homeowners, leaving them more money to spend on the cost of living and monthly repayments. As their net income grows, so do their options for refinancing their home loans.

Current homeowners who allocate their entire stage-three tax cut savings to their mortgages could save thousands of dollars and reduce their loan term by up to six years.

The tax cuts could also benefit potential buyers sitting just outside their ideal borrowing capacity, as the extra income can be directed towards saving for a deposit.

State-specific initiatives

The ACT and Queensland offer government-funded mortgage relief programs for homeowners facing short-term, severe financial hardship. These schemes provide interest-free loans to cover arrears and some future payments, offering crucial support during difficult times.

Each has its own stringent eligibility requirements. For further details, contact the ACT Revenue Office or the Queensland Department of Housing.

Some other states and territories also have resources available for dealing with mortgage stress:

- New South Wales: Legal Aid

- Northern Territory: Homeowner assistance

- South Australia: Department of Human Services

- Western Australia: Legal Aid

What can I do if I’m under mortgage stress?

It’s always possible to find yourself in deep financial water. If you’re going through mortgage stress, here are some ways you can grab a life jacket:

Cut down on expenses

We won’t gaslight you and say your mortgage stress comes down to your spending, because there are a lot of macroeconomic forces at play here.

But it would be remiss of us if we didn’t add this tip in! Cutting down on expenses – especially in a climate where cost-of-living pressures are palpable everyday – can help ease mortgage stress. It’s one of the easier things to do and you can start doing it today.

For example, you could reallocate your short-term travel funds or weekly splurge budget into monthly home loan repayments. At least to ride out these uncertain times.

Consolidate your debts

If you have other debts like a car loan, personal loan, and credit cards, you could think about consolidating them.

Debt consolidation has its merits. You can reduce your total monthly repayments and you only have one loan to think about. That makes it easier to keep track of your repayments (so you don’t miss multiple deadlines) and gives you an idea of when you’ll go debt free.

You can also take advantage of lower interest rates in home loans compared to those from car loans, credit cards, and other types of debt.

Seek assistance programs

Consider speaking to a qualified financial adviser for options and various assistance programs. Get in touch with your lender’s financial hardship support team. Check the resources available in your state or territory.

You can also go to the Australian Banking Association’s financial assistance hub or contact the National Debt Helpline to get guidance from their financial counsellors.

Speak to your broker and lender

Think about talking to a broker to make sure your loan structure works for you. Make sure you understand how loan features like offset accounts, fixed rates, and interest only periods work in the short and longer term.

You can also look into home loan repayment deferral or hardship variation with your lender. It’s important to check whether you’re eligible, and also to make sure you understand the long-term implications.

Consider refinancing

You could possibly refinance or restructure your home loan with another lender.

It could give you a higher chance for a competitive rate. After all, it’s no secret that lenders charge existing customers slightly higher rates than what they offer to attract new customers (ah, the loyalty tax).

Consider picking up the phone to ask your lender how to get more competitive interest rates. And if you don’t get the green light, shop around for other home loan options.

Helpful tip

Helpful tip

Whether you’re feeling the pinch or just trying to stay ahead, it pays to check in on your loan regularly. Don’t wait for the RBA to move or interest rates to spike. Look for ways to lower your rate, trim your repayments or cut costs now.

Mortgage stress is tough, but some foresight (and the right support) can make all the difference.

Sam Hyman

General Manager – National Sales, Aussie

Where can I find and compare home loans?

If you think refinancing is a sound advice, you can start by comparing home loans. iSelect has partnered with Aussie to help you compare from over 25 lenders online.

Get started on comparing home loans today!

Find a home loan by comparing with iSelect’s trusted partner, Aussie.

iSelect is the trading name of iSelect Mortgages Pty Ltd (ABN 86 148 217 181). iSelect Mortgages Pty Ltd is a credit representative (Credit Representative 400540) of Lendi Group Distribution Pty Ltd (Australian Credit Licence 246786). iSelect provides a referral to Lendi Group Pty Ltd, a Credit Representative of Lendi Group Distribution Pty Ltd (Australian Credit License 246786). iSelect Mortgages Pty Ltd receives a commission from Lendi Group Distribution Pty Ltd, the licensee for each new customer account created and for each home loan submitted through this service.