.svg)

Accidental Damage Insurance

Accidental Damage Insurance

Written by

Tina Sendin

Edited by

Laura Crowden

Reviewed by

Adrian BennettCompare home and contents insurance the easy way

Save time and effort by comparing a range of home and contents insurance policies with iSelect

What is accidental damage insurance?

Long story short

Accidental damage insurance is your safety net for oops moments

Accidental damage insurance steps in when life gets messy – think wine spills on the couch, cracked TV screens, or coffee all over your laptop.

Surprise, unintentional loss or damage is generally covered

From tech mishaps and DIY disasters to pet chaos and clumsy moments, you’re sorted for unintentional damage to the important stuff.

Several things aren’t necessarily in the menu

Intentional damage, tenant-related mishaps, or tech issues like viruses won’t make the cut. Items like cash, phones, and work gear are off the list too.

It might cost more, but it might also be worth the extra headspace

This extra layer of peace of mind? Not as pricey as replacing a sofa or gadget. Cost will vary based on things like your location and belongings.

What is accidental damage insurance?

If you’re someone who’s prone to little disasters – or just living in a household with kids, pets, or slightly clumsy mates – accidental damage insurance might be the extra protection you never thought you needed. It’s an optional cover designed to bail you out after sudden and unexpected damage to your belongings or home.

Spill coffee on your laptop during a blue Monday meltdown? Drop your phone face down on the driveway? This is when you’ll thank your past self for getting accidental damage insurance.

Unlike your standard home and contents insurance – which mainly takes care of big-ticket issues like storms, theft, and fire – this one’s all about what anyone at home accidentally does (yes, including the overly curious cat).1For more information, see Moneysmart – Home insurance

Of course, ‘accidentally’ is the operative word here. Insurers generally define ‘accidental damage’ as spur-of-the-moment, unintentional loss or damage.

Accidental damage insurance is peace of mind for those random ‘oops’ moments that just sort of… happen.

Does standard home and contents insurance cover accidental damage?

Accidental damage insurance is typically an optional add-on or extra to your home insurance policy.

Your standard home and contents insurance is more about the big stuff, like protecting your house from a raging storm or replacing stolen goods. But your carpet after that red wine disaster? Or TV that got a little too close to your toddler’s toy hammer? Not covered.

Helpful tip

Helpful tip

Read the product disclosure statement (PDS) on your current policy. If something doesn’t make sense, just give your insurer a call and ask them to clear it up. You might find out you’re already covered for accidental damage, or spot a few gaps you’ll want to sort out.

Adrian Bennett

General Manager for General Insurance

What can accidental damage insurance cover?

Every insurer’s policy is a bit different, but here’s the gist of what accidental damage insurance typically includes:

- Electronics copping it: Dropped your laptop? Cracked an iPad? Smashed your TV screen? Yep, usually covered.

- Spills and stains: Merlot, coffee, or kids’ textas that somehow ended up on your couch are generally taken care of.

- Fragile stuff: Broken vases, glass doors, mirrors – these kinds of accidents are usually sorted.

- DIY fails: Damage from your weekend DIY project gone wrong. You gave it a crack – literally.

- Pets being… pets: Crazy pets playing bull in a china shop? You’re covered if your chocolate lab destroys your curtains or knocks over the fishbowl.

Of course, always double-check your product disclosure statement or PDS to be sure!

What does accidental damage insurance NOT cover, usually?

Not everything’s covered or considered ‘accidental’. Here’s what accidental damage insurance usually won’t protect you against:

- Normal wear and tear: Sorry, those worn-out carpets are on you.

- Slow leaks and dampness: That stuff creeps in too gradually to count as ‘accidental’.

- Things done on purpose: If your mate threw the remote on your TV after a ripper footy grand final, you’re out of luck – no claims there.

- Tenant troubles: Damage caused by tenants living in a property you own isn’t covered either (unless you have landlord insurance).

- Dodgy cleaning jobs: Used harsh chemicals (other than the usual household stuff) and wrecked something? That’s unfortunately on you.

- Tech disasters: Computer viruses or corrupted files? Insurance won’t step in for those.

- Burn marks: Think cigar, cigarette, or pipe burns – yep, not covered.

- Renovation mishaps: Damage caused during construction or major reno projects is usually excluded.

And here are the kinds of items typically not covered for accidental loss or damage:

- Cash or financial goodies: Cash, cheques, gift cards, and anything similar don’t count.

- Clothes and accessories: If something happens to your wardrobe, don’t count on insurance.

- Your phone: Mobile phones are usually excluded. Brutal, right?

- Pools and spas: Yep, damage to your backyard oasis isn’t often part of the deal.

- Work gear: Things used for business, trade, or your profession aren’t covered.

- Sports stuff or bikes in action: If your gear (like sporting equipment or your bike) gets damaged, that’s usually a no-go for accidental damage claims.

Is accidental damage cover worth it?

Short answer: It’s totally up to you.

Here’s the long answer: If you’ve got kids, pets, or pricey stuff you’d rather not risk replacing out of pocket, it’s probably worth every cent. If you’re living the ultimate DINK (double income, no kids – or pet) life, you might not need it.

But if you’re a DINK couple who throw parties every so often, then it’s worth looking into one!

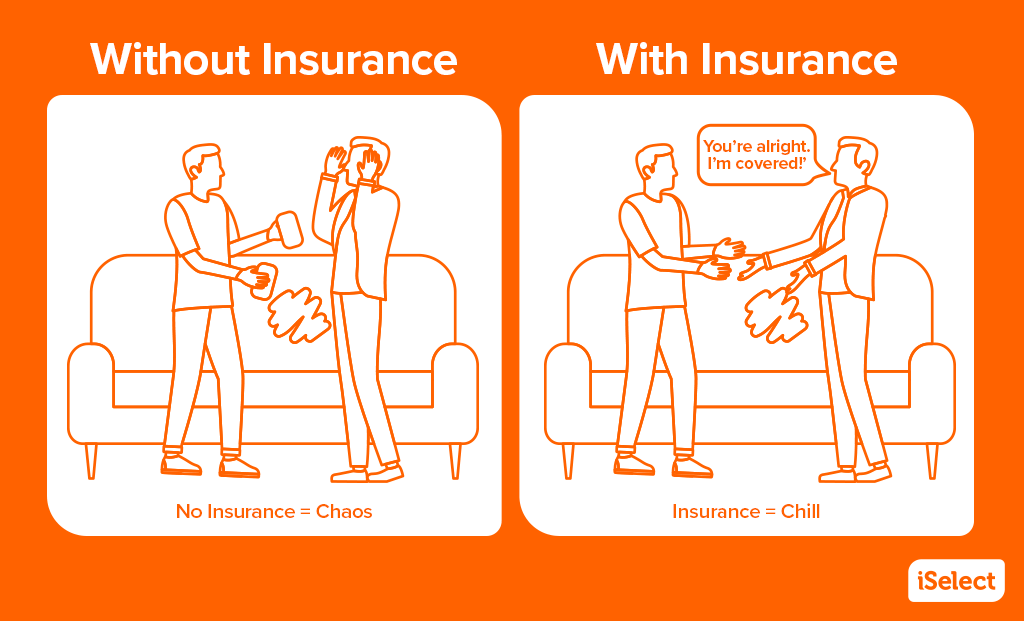

Picture this. You’re throwing a housewarming party. Your mates are over, enjoying a couple of cold ones, when someone’s wine glass topples over your newly delivered couch.

Without accidental damage insurance, you’re playing the blame game and footing the bill for cleaners – or a new couch altogether.

With it? No dramas – it’s all a funny story to laugh about at your next house party.

How much will accidental damage insurance cost me?

Now to the money side of things. Adding accidental damage insurance to your policy isn’t too pricey, but it does depend on a few factors like your location, the value of your stuff, and who you’re signing up with.

Also note that some providers apply a certain excess amount when claiming for accidental damage. The dollar value depends of course on the insurer and the type of excess – whether it’s basic, accidental damage, or special for example. It’s always a good idea to ask the insurer about the excess that’s linked to this optional cover.

Does accidental damage cover still apply if I take my contents out of my home?

Dropped your laptop while working in a cafe? Whether you’re covered for accidents beyond your home depends on the specifics of your policy.

Most of the time, if you want to have coverage for stuff that leaves the house, you’ll need portable contents insurance instead. You can always ask your insurer about getting it along with accidental damage if it’s important for your lifestyle.

What are some things to consider when buying accidental damage insurance?

Before signing up, here’s what you might like to suss out first:

- Your risk levels: Got pets, kids, or live for a bit of DIY? Consider your risk factor.

- The PDS: Policies vary heaps so always read the details in the product disclosure statement before you commit.

- Bundled discounts: A lot of insurers will chuck in discounts if you package multiple policies together.

- Lifestyle fit: Travel often? Pair this with portable contents coverage.

- Customer reviews: Not all insurers deliver the goods. Pick one with solid customer feedback.

iSelect can help you compare home insurance

Look, accidents happen. But they don’t have to drain your bank account or ruin your day. Accidental damage insurance could save you a whole heap of stress and cash down the road.

Curious about your options? Don’t hang around waiting for that wine glass to tip on your immaculate couch! iSelect can help you explore policies today.

Get started on comparing home and contents today!

Save time and effort by comparing a range of home and contents insurance policies with iSelect

iSelect General Pty Ltd (ABN 90 131 798 126. AFSL 334115) has partnered with Compare the Market (ABN 83 117 323 378. AFSL 422926) to compare a range of home insurers and policies. Not all providers in the market or all policies offered by the partners are compared and not all policies or special offers are available to all customers.

A number of our participating general insurance brands are arranged by Auto & General Services Pty Ltd ACN 003 617 909 on behalf of Auto & General Insurance Company Limited 111 586 353, both of which are related entities of iSelect Limited. Our relationship with those companies does not impact the integrity of our comparison service. Click here to view iSelect’s range of providers.

Any advice provided by iSelect is of a general nature and does not take into account your objectives, financial situation or needs. You need to consider the appropriateness of any information or general advice iSelect gives you, having regard to your personal situation, before acting on iSelect’s advice or purchasing any policy. You should consider iSelect’s Financial Services Guide which provides information about our services and your rights as a client of iSelect. iSelect receives commission for each policy sold that is a percentage of the premium or a flat fee. Ask us for more details before we provide you with any services.