.svg)

Cost to Refinance Your Home Loan

Cost to Refinance Your Home Loan

Written by

Luke Carlino

Edited by

David Rayfield

Reviewed by

Sam HymanCompare home loans the easy way

We partnered with Aussie to help you compare home loans from over 25 lenders and over 2,500 home loan products.

Can I Save Money by Refinancing?

Are you thinking about refinancing your home loan? It might help you save quite a bit of cash on your mortgage repayments—but it all depends on your personal situation and current loan setup.

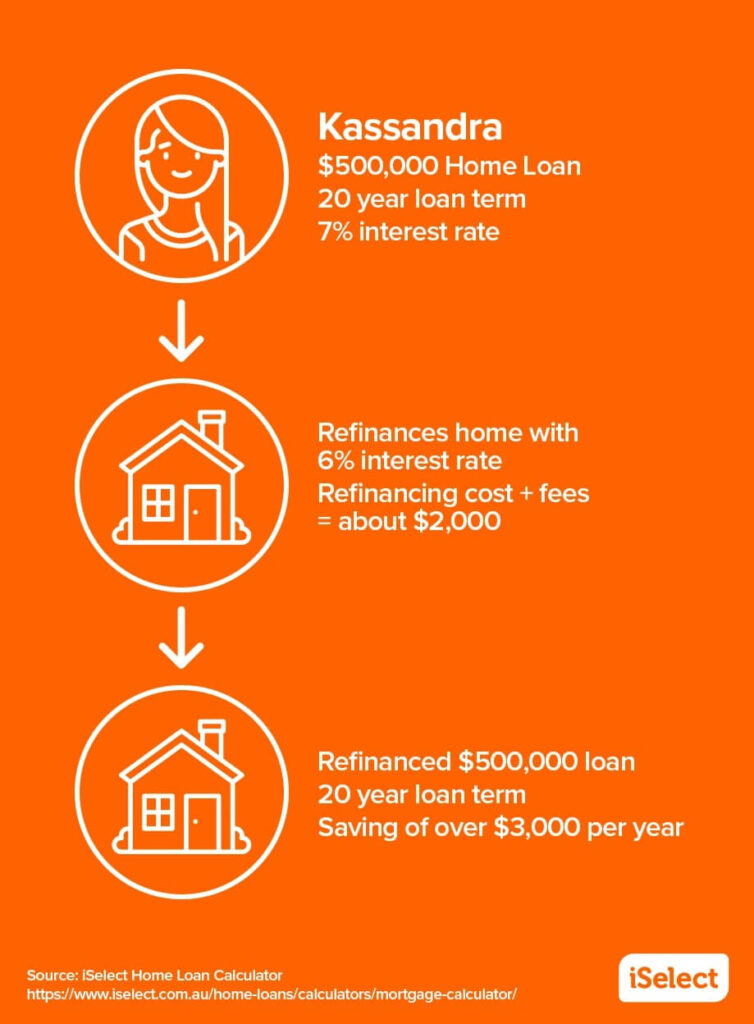

First off, let’s take Kassandra as a quick example. She’s paying off a $500,000 home loan with a seven per cent interest rate. Then, one day, she decides to refinance her home with a lender offering a six per cent interest rate. With mortgage discharge, application and valuation fees, she knows she’s looking at about $2,000 in refinancing costs, but with twenty years left on the loan, she’ll be saving over $3,000 each year.

Of course, not everyone’s in Kassandra’s situation. Some people might also have a lot of debts to juggle—like multiple, high-interest credit cards. Refinancing your mortgage could help you pay off these cards by rolling all that debt into a loan with lower interest. Of course, this can also mean higher repayments, so it’s not something you should rush into without careful consideration.

Another reason people refinance their home loan is because their financial situation changes. Maybe they want to slash their monthly repayments by snagging a more competitive rate. Maybe their current loan lacks certain features, like redraw options, offset accounts, or flexible repayments. Or, they might be nearing the end of a fixed-rate term, and now they’re on the prowl for a variable home loan that meets their needs. Everyone’s situation is different.

What fees can I expect to pay?

Let’s dissect the home loan makeover game, where potential savings meet the hurdles of fees. Here is a breakdown of each fee you might encounter on your financial adventure.

Break Fees

- What’s the Deal: Especially crucial with fixed-rate home loans.

- Why It Matters: If you break up with your current lender during a fixed rate period, expect a hefty fee. How much depends on the length and size of your loan, and your lender but bear in mind, it could be as much as tens of thousands of dollars.

Application Fees

- What’s the Deal: The cost of signing up with a new lender.

- Why It Matters: This fee can cost up to $1,000, but keep in mind it also varies from lender to lender.

Discharge Fees

- What’s the Deal: Covers the admin involved in closing your old loan.

- Why It Matters: It’s pretty darn necessary from a legal standpoint; it might also set you back $150-$500.

Valuation Fees

- What’s the Deal Your new lender will probably want to assess your home.

- Why It Matters: It costs about $100-$600 and will tell your lender whether your house has increased or decreased in value.

Lender’s Mortgage Insurance (LMI)

- What’s the Deal: This might apply if you own less than 20% of the property.

- Why It Matters: Lender’s Mortgage Insurance can cost about 1-3% of your home’s value, which can add up to quite a bit!

Administrative Fees

- What’s the Deal: Your new loan might also come with a regular admin fee.

- Why It Matters: This can include monthly service fees of about $5-$15 to annual fees of $300-$400.

Where can I find and compare Home Loans?

It’s a smart move to give your home loan a little check-up every 12 months or so just to make sure it’s still doing its job for you. Your home loan is like the heavyweight champ of your investments, so you want to make sure it’s the right fit. Lucky for you, we’ve got a nifty Refinancing Calculator online. Pop in the details of your current loan, and let’s see how it measures up.

iSelect has teamed up with Aussie, for comparing a bunch of providers in the market. Use our slick online tool to size up those home loans.

Get started on comparing home loans today!

Find a home loan by comparing with iSelect’s trusted partner, Aussie.

iSelect is the trading name of iSelect Mortgages Pty Ltd (ABN 86 148 217 181). iSelect Mortgages Pty Ltd is a credit representative (Credit Representative 400540) of Lendi Group Distribution Pty Ltd (Australian Credit Licence 246786). iSelect provides a referral to Lendi Group Pty Ltd, a Credit Representative of Lendi Group Distribution Pty Ltd (Australian Credit License 246786). iSelect Mortgages Pty Ltd receives a commission from Lendi Group Distribution Pty Ltd, the licensee for each new customer account created and for each home loan submitted through this service.